Authors: R. Matthew Hedges1, David Hughes2

1School of Continuing Studies, Sports Industry Management, Georgetown University, Washington D.C., USA

2School of Continuing Studies, Sports Industry Management, Georgetown University, Washington D.C., USA

Corresponding Author:

R. Matthew Hedges, MPS

295 Durham St.

Unit F

Lake Oswego, Oregon 97034

ramonmhedges@gmail.com

541-727-1008

1R. Matthew Hedges, MPS, is a graduate of Georgetown University’s School of Continuing Studies and studied Sports Industry Management. In light of the current sports franchise ownership market and the lack of diversity thereof, Hedges’ interest includes finding a pathway to a more inclusive sports ownership structure.

2David C. Hughes, Ph.D., M.Ed., is an adjunct professor at Georgetown University’s School of Continuing Studies. His specialties include esports, diversity, equity, and inclusion within sports management, and sports technology.

Restructuring NFL Ownership, A New Way Forward

ABSTRACT

Racial discrimination still exists in the NFL today. What has been referred to as a modern-day plantation, NFL franchises have insufficient diversity at the ownership level as well as in the top front office positions. NFL franchise owners have illimitable power and are averse to a 21st-century progressive society. The league is a multi-billion-dollar enterprise that is owned and operated by 32 franchise owners. Although the NFL is the behemoth of the sports industry, there are ingrained systemic issues. Instead of putting a band-aid on a bullet wound, the NFL must address the diversity concerns with strategic initiatives to overcome the deficiencies. A comprehensive top-down structural reformation is required to alter the ownership level. With the introduction of private equity funds, amending the Rooney Rule to include limited partners, and modifying the relationship between NFL franchises and their respective local governments, diversity within senior executives will advance. While the 32 owners have tightly held the reins of the league, a revolution must transpire.

Key Words: NFL Ownership, Diversity in the Workplace, Social Reform, Private Equity, Rooney Rule, Equal Opportunity

INTRODUCTION

The National Football League (NFL) has had a history of racial segregation dating back to the 1930s. Rumored to be a gentleman’s agreement between the current owners, all Blacks be barred from playing in the league. Following in Major League Baseball’s (MLB) footsteps, the NFL did not have one black athlete on the playing field from 1933 to 1946 (1). Succeeding this period, all owners denied the existence of such a ban, including Art Rooney, the then-owner of the Pittsburg Pirates, currently known as the Pittsburg Steelers. Ray Kemp, an African American starting offensive tackle, was cut from the Pirates in 1933 following just two games into the regular season. “It was my understanding that there was a gentlemen’s agreement in the league that there would be no more blacks,” Kemp stated in an interview with Bob Barnett (1). George Marshall, the owner of the former Washington Redskins, now Washington Commanders, believed to instigate the racial ban. The Redskins franchise was the last to desegregate, holding out until 1962 (2). Following Marshall’s death in 1969, his estate was put toward establishing the Redskins Foundation. According to Ta-Nehisi Coats of The Atlantic, the Redskins “Foundation was stripped from spending money on ‘any purpose which supports or employs the principle of racial integration in any form” (3). Ironically, nearly 20 years following Marshall’s death, Doug Williams was the first black quarterback to win a Super Bowl and did so in a Redskins uniform in 1988 (3).

BACKROUND

Diversity in the Workforce

Diversity in the workplace, particularly in a leadership position, has been controversial in the United States ever since the country’s establishment. Whether consciously or subconsciously, predominately white males from affluent backgrounds have held the keys to authority and influence at all levels of society. Due to white males holding most leadership positions, prejudice has been cultivated by negative stereotypes surrounding diversity at the management level. Optimistically, much is progressing in the United States and globally, as an increasing representation of women and racial and ethnic minorities are starting to transform the narrative (4). Diversity, equity, and inclusion are directly correlated with a more robust and complex organization from top to bottom. Adding organizational diversity to the workplace can lead to more effective communication across employees and further increase productivity levels (5). Utilizing varying beliefs and viewpoints allows an organization to be readily available to bring about change and growth.

Rooney Rule Chronicle

In December of 2003, the 32 owners of the NFL voted on what is now known as the Rooney Rule. Introduced and brought to light by longtime civil rights lawyers Cyrus Mehri and Johnnie Cochran, the Rooney Rule “aims to increase the number of minorities hired in head coach, general manager, and executive positions” (6). The original rule stated that each franchise must interview a minority candidate for each head coaching vacancy. Since 2003, there have been several revisions to the rule modernizing the policy to try and promote more diversity in executive-level positions of the franchise. A recent amendment from October 2021 “requires every team to interview at least two external minority candidates for open head coaching positions and at least one external minority candidate for a coordinator job. Additionally, at least one minority and/or female candidate must be interviewed for senior-level front office positions (e.g., club president and senior executives)” (6).

In March 2022, the NFL announced additional requirements associated to the Rooney Rule. Dating back to the mid-20th century, people of color were stigmatized for lack of intelligence for skilled offensive positions; the NFL has prioritized increasing diversity among its offensive coaches. White offensive-minded coaches have seen preferment when head coaching opportunities become available compared to their defensive counterparts (7). In response, each team must hire an offensive assistant coach of minority status before the 2022 season (8). This coach must work alongside the head coach and offensive staff to enhance the minority hiring pool in future years (9).

Although, throughout the near 20 years of the rule’s installation, there have been numerous instances of workarounds and sham interviews. While the statute has proven to promote change and progress towards equitable opportunity, many franchises have ignored the policy throughout its short history. The use of sham interviews as workarounds violates the ethical element of the entire purpose of the rule. “The granting of coaches of color ‘token’ interviews is in direct opposition to the intent of the Rooney Rule” (10).

An example of the unethical sham interview tactic is currently at the center of a class-action lawsuit involving Brain Flores and two different NFL franchises. Flores, a former black head coach of the Miami Dolphins, is suing the NFL and its 32 franchises. Alleging racial discrimination in hiring processes, Flores is citing the New York Giants and the Denver Broncos as teams that hosted him as a Rooney Rule interviewee instead of a legitimate candidate. While the NFL is continuously trying to sweep all negative publicity under the rug, it is apparent that long-standing racial prejudices still exist in the NFL.

The Flores v. NFL case is currently in litigation.

NFL Ownership Structure

Several requirements need to be completed before becoming a general partner of an NFL franchise. To be eligible, the proposed person or consortium for ownership needs to formally write an application to the commissioner outlining their intentions for the respective franchise (11). The league does not allow corporation partnerships or funds to own a franchise, only individuals and preferably single owners. Scott Soshnick of Sportico mentioned that the NFL favors a single owner putting all of the liquidity in themselves versus a much larger group prone to conflict (12). After a thorough investigation by the league and Commissioner into the applicant, it then goes to a vote. A passing three-fourths majority for each individual applying for ownership (11). A majority owner must pay at least 30% of the agreed-upon price to become the general partner with the approval to proceed. If the franchise is not paid in full, the remaining balance must be paid through the other stakeholders within the consortium labeled as limited partners (13).

Bob Reif, the former Chief Marketing Officer for the then St. Louis Rams, mentioned that the league office and the current owners are seldom blindsided about a new prospective owner. There is a narrow group of people predisposed to purchasing a team (14). With all of the bylaws and obligations that a new owner has to abide by, one thing is certain; the new prospective buyer must receive the NFL’s blessing. Anthony Di Santi, Head of Global Sport Finance at Citi Private Bank, stated, “The buyer and seller can agree on the price, but if the league doesn’t like the buyer or doesn’t like the price, it’s not going to happen” (14).

Throughout the league’s history, NFL ownership is a hallowed membership that rarely goes for sale. One of the primary reasons for the lack of ownership turnover is that the franchise is predominately put into an irrevocable family trust. By passing the organization down from generation to generation, keeping it within the family forms an enormous tax benefit (15). Suppose the principal owner passes away and the franchise is in the trust, the inheritor(s) receives a significant reduction or can eliminate the severe estate and gift taxes on the asset. Integrating rising franchise valuations with the massive tax write-off, NFL owners and their families will continue creating an apparent dichotomy.

As of March 28th, 2022, the NFL and its 32 owners revealed a newly formed Diversity Advisory Committee. The committee comprises experts across multiple industries, including academia, corporate business, diversity, equity and inclusion, and legal. The six-person panel will provide oversight and recommendations to the franchises and their executive teams, involving ways to increase diversity and inclusion strategies and initiatives (6). This type of guidance will allow a third-party group, a blend of a directorate and a consultancy firm, to evaluate every franchise. Five of the six committee members are either black or female (see Appendix 2 for the NFL Diversity Advisory Committee).

The TIDES Report

The TIDES report is produced annually by The Institute of Diversity and Ethics in Sport (TIDES) at The University of Central Florida. The TIDES report highlights diversity and inclusion statistics across several professional franchises, leagues, and NCAA conferences, featuring owners, front office executives, coaches, and players.

In the 2021 Racial and Gender Report Card for the NFL, The TIDES Report gave the NFL a failing grade regarding diversity and gender at the ownership level. There are only two principal owners of minority status in the NFL, with neither one being of African American descent. Kim Pegula of the Buffalo Bills is an Asian-American female, and Shahid Khan of the Jacksonville Jaguars is a Pakistani-American (16).

Regarding the front office of NFL franchises, The TIDES Report gave the NFL failing grades for the President and CEO levels. Across the entire league, there are only three individuals of minority status in this leadership position. With only 9.4% of team Presidents and CEOs of minority status, the Rooney Rule was updated to include front-office executives (6). The three individuals of minority status are all Presidents of the respective franchises, Kim Pegula of the Bills, Hymie Elhai of the New York Jets, and Jason Wright of the Washington Commanders.

The TIDES graded racial diversity in the NFL as an A+ for players, assistant coaches, and league office employees. An A- was conferred for professional team staff, a B for C-Suite executives, a B+ for senior administrators, and a C+ for head coaches, team general managers, and team vice presidents. Lastly, an F was given regarding team owners and team Presidents and CEOs (16). There is a direct contrast of race and people of minority status between players and their assistant coaches with the team owners and Presidents and CEOs. Dr. Richard Lapchick, the primary author of the TIDES, stated that “there needs to be a change in the continued dissimilarity in racial and gender hiring practices between the NFL League Office and the 32 teams” (16).

At the start of the 2021 season, one person of color and seven women were principal owners. However, Kim Pegula is the only principal women owner with at least 50% of team ownership, accompanied by her husband Terry when purchasing the Buffalo Bills in 2014. “To the extent that women own teams…they are largely the wives, widows, or daughters of men who purchased the team” (17). Whether through marriage or inheritance, operating woman owners is not the norm.

The NFL and its 32 ownership groups have special committees that are responsible for various subjects concerning the league. One of the committees is the Workplace Diversity Committee. The principal objective of this committee is to “increase employment opportunities and advancement for minorities and women” (6). The Fritz Pollard Alliance is a nonprofit organization that advocates for diversity and employment equity within the NFL. The Fritz Pollard Alliance and Workplace Diversity Committee work diligently through consultancy efforts (see Appendix 3 for the NFL Workplace Diversity Committee).

Recent Ownership Transactions

Ownership transactions are vital to the health of the league as a whole. Due to the scarcity of turnover in franchise ownership, each transaction can have ripple effects across the entire league. General partners of NFL organizations infrequently put a team for sale voluntarily. Typically, franchises only come for sale due to fatality, or the owner is ostracized by their 31 other colleagues. The Carolina Panthers and the Denver Broncos were the two most recent ownership transactions.

Due to the recency of the Denver Broncos transaction, this section has been amended to outline the entire sale process, including prospective bidders and the eventual new owner.

The Carolina Panthers

In the late months of 2017, the founder and owner of the Carolina Panthers, Jerry Richardson, announced his plans to sell the franchise due to the rise of alleged workplace misconduct reports. Racial slurs and sexual harassment claims were brought forth against Richardson (18). By May 2018, the transaction was complete, and David Tepper, an American hedge fund manager, bought the Panthers organization for a then-record sale price of $2.2 billion (19). Between the time Richardson put the team for sale, and when Tepper officially bought it, the NFL finance committee proposed and passed a new policy. The committee changed the debt limits from $250 million to $350 million to help entice more individuals. Since the sale of the Carolina Panthers, the NFL again has raised the debt limit from $350 million to $500 million during the COVID-19 pandemic to provoke ownership turnover and entice organizations to leverage debt for franchise improvements.

The Denver Broncos

The Denver Broncos were known to eventually hit the market in search of a new owner since the mid-2010s when the then-owner, Pat Bowlen’s health started to decrease, and he ultimately passed away in June 2019. According to Sportico’s NFL franchise valuations before the sale, the Denver Broncos were valued at $3.8 billion (20). The sale was held as an auction due to the organization’s general partner passing away. The bank had a fiduciary obligation to award the highest bidder. When comparing the Panthers and Broncos transactions, Richardson did not have a fiduciary duty to receive the most money from a potential bidder. The Panthers conducted their transaction as a private sale.

Before Denver’s sale, on March 28th, 2022, following an owner’s meeting, the NFL and its 32 owners issued a statement welcoming the possibility of an ethnic minority owner joining their ranks. While this prompted a discussion of accepting a black person in their presence, it also came with the stigmatization of permitting another person of minority status into their sacrosanct society.

During the sale process, two imminent black bidders garnered publicity, Bryon Allen and Robert F. Smith. Commissioner Roger Goodell had been vocal about seeking a diverse owner for the Denver Broncos. “We would love to see a diverse owner of the team…We think that would be a really positive step for us and something we’ve encouraged. And one of the reasons we’ve reached out is to find candidates who can do that” (20). When Goodell publicly stated the need for a diverse individual at the ownership level, specifically at the general partner level, it further proved the notion of white supremacy ruling NFL franchises. Allen and Smith were considered ideal candidates for leading an NFL franchise and would have been the first black principal owner in NFL history.

In the end, Rob Walton rose victorious and bought the Denver Broncos for a record-setting sale price of $4.65 billion (21). Walton, the highest bidder, purchased the franchise from the Pat Bowlen family after the NFL owners and league finance committee unanimously approved the transaction on August 9th, 2022 (22). Walton acquired his $59.5 billion fortune as heir of the Walmart family (21). The 78-year-old white male spent most of his illustrious business career as Chairman of Walmart. Along with Walton, his daughter and son-in-law, Carrie Walton-Penner and Greg Penner are included in the ownership group.

A crucial aspect of the Broncos sale and most transactions in professional sports ownership is that the impending bidder must have the required amount of money in liquid cash ready to purchase. Walton paid a hefty price tag to own a controlling interest. At a minimum of a 30% stake in the franchise and a purchase price of $4.65 billion, Walton paid at least $1.395 billion in cash to be considered the majority owner. The remaining sum comes from a combination of either debt borrowing or limited partner investors. According to Mike Ozanian of Forbes, the NFL has increased the debt limit from $500 million to $1 billion for someone buying the controlling interest in a franchise (23). This debt limit increase directly relates to the skyrocketing franchise valuations and the expected upsurge in the coming years.

Franchise Valuations

Based off the 2022 Sportico NFL Franchise valuations, the average NFL franchise is valued at $4.14 billion. According to Kurt Badenhausen of Sportico, the NFL is the most valuable league across all professional sports (24). The top four wealthiest owners in the NFL are Rob Walton of the Denver Broncos, the Paul Allen Trust of the Seattle Seahawks, Clark Hunt of the Kansas City Chiefs, and David Tepper of the Carolina Panthers. Chairwoman Jody Allen manages the Paul Allen Trust, the sister of Microsoft co-founder Paul Allen, who has a reported trust worth $20.3 billion (25). In addition, the average collective net worth of the owners is estimated to be $4.86 billion. In comparison, Mark Davis of the Las Vegas Raiders and John Mara of the New York Giants have the smallest net worth, valued at around $500 million (26).

The prosperity of the NFL franchise valuations stems directly from the ever-escalating broadcast media rights deals (17). In 2021, the NFL reached a record-shattering agreement with five different media companies, combining to generate over $110 billion over 11 years (27). The NFL has a shared revenue model, divvying up the national television contracts to its 32 franchises regardless of each franchise’s win-loss record or market size. While some owners and franchisees may try and dispute league-wide revenue-sharing practices, it subsequently allows the league to display competitive balance on and off the field. Due to the most recent broadcast contract set to take effect in 2023, which was an 80% increase from its previous deal, the franchise valuations jumped a staggering 14% over the past two years alone (23).

The professional sports industry, which includes the other four major sports leagues, has also seen rapid appreciation in the last two decades. The National Basketball Association (NBA), on average, has seen the most growth, with a total return of 852% (28). U.S. professional sports franchises continue to operate as premium, scarce assets that continue to appreciate year-over-year (29).

While the NFL continues to be the most profitable professional sports league, some growing pains may come with franchise valuations soaring at an all-time high. As seen with the Denver Broncos, there is a risk for the NFL that their standards are starting to become out of reach for even the wealthiest individuals, let alone individuals of minority status. According to Badenhausen, there are plenty of billionaires interested in sports ownership, particularly the NFL, due to its low risk and high returns (24). The issue, however, is that franchise valuations are exponentially rising, and the number of people who can place a valid bid is becoming infinitesimal.

Private Equity in Sports

Institutional funds have long been ostracized from professional sports from an ethical standpoint because they do not want to complete the notion that they are profit-generating behemoths. Now that sports entities have profitable annual returns and skyrocketing valuations, private equity funds see an opportunity primed for long-term investment. In contrast, the current owners see a liquefiable exit strategy.

As a result of the COVID-19 pandemic, the sports industry has entered a new era of sports ownership. Due to the uncertainty of the economic downturn spurred on by the 2020 pandemic, sports leagues and franchises turned to private equity funds to ensure financial assurance at a time of need. Before 2020, private equity in sports was slowly gaining exposure but quickly became a hot commodity. According to Browndorf, sports has been an attractive investment avenue due to the escalating franchise valuations (30). Over the last two decades, the four major U.S. sports leagues have outperformed the four major stock indexes on annual growth rates (30).

Digging further into the relationship between sports franchises and investment funds, several parallels allow the unique partnership to flourish. The soaring valuations are predominantly due to broadcast partners’ multi-billion-dollar media rights contracts. Naturally, these contracts last anywhere from seven-ten years, which directly corresponds to a standard investment fund holding period that guarantees a positive return (30). Secondly, the general partners of NFL franchises and other professional sports team owners are constantly looking for limited partners that only want to own passive stakes in the franchise. This bodes well for private equity funds. Even though private equity funds typically have a managing director, there has not been a push for fund managers’ decision-making rights (30). Private equity investments allow general partners not to carry the burden of the total price for the franchise but still hold full operational authority and voting power.

Private equity has been initiated across the four other major professional sports leagues in the United States, Major League Soccer (MLS), National Hockey League (NHL), Major League Baseball (MLB), and, most notably, the NBA. By opening the doors to private equity investors, these leagues have increased the overall liquidity pool for minority investors and drove the valuations to greater unforeseen heights (30). The NBA and its vastness are one of the only leagues that NFL insiders often compare themselves to. They introduced private equity at the pinnacle of the 2020 pandemic seeking an influx of cash and stability at the ownership level. Dyal Capital Partners, a first-of-its-kind dedicated sports investment firm, was the original private equity group allowed access to invest in NBA franchises. Not long after seeing the success and operational efficiencies of Dyal implementing itself into the NBA, Arctos Sports Partners, and Redbird Capital Partners found success. The NBA has two requirements when it comes to equity investors:

- An equity group cannot own more than 20% of a single franchise.

- No franchise can collectively have more than 30% of its ownership group from private equity investors (28).

Ownership in a sports franchise operates as an illiquid asset. Mike Davey, a limited partner in a Serie A Italian football club revealed that the only time an owner’s, majority or minority, stake is worth the appraised value is when a potential buyer shows interest and a transaction occurs (31). As an owner, one typically does not see any dividends or profits associated with financial success (31). Most organizations reinvest the profits from the year before to supply cash flow for future years. Allowing private equity firms to invest in sports franchises generates a potential exit strategy for limited partner investors.

Publicly Funded Stadiums

For many decades, public versus private financing of stadiums has been at the forefront of sports economists, franchise owners, and city and state officials. The contentious topic is whether or not a professional sports franchise and its billionaire owner(s) should pay for its own stadium upgrades. The alternative is to place the burden on local and state taxpayers to finance the multimillion, if not, multibillion-dollar, price tag. Arguments can be had for each side, resulting in an inconclusive resolution. The two noteworthy examples are the Buffalo Bills and the Los Angeles Rams. Stam Kroenke, the owner of the Los Angeles Rams, built So-Fi Stadium in Inglewood, Ca. for a record $5 billion-plus, all privately funded. On the flip side, as of March 2022, the Buffalo Bills and the Pegula family were approved for a record-setting $850 million of public taxpayer money for a new stadium in Erie County, New York (32).

Andrew Zimbalist and Roger Noll, well-renowned sports economists, have long debated the topic of professional sports franchises and their economic impact on the community they are located in. One of the primary quarrels associated with public funds supporting sports franchises is that the community is negatively affected (33). The economic impact of a sports franchise on the city does not necessarily boost the return as most people expect. Sports teams are private enterprises that yield a large monopoly over their home cities, allowing them to extract millions of dollars in local subsidies without displaying any spillover gains for the public good (34). The economic concept of ‘socializing costs and privatizing profits’ (35) is what franchise owners have been displaying by using public funding. At the same time, little evidence supports those returns being spent back on the local economy. Very rarely are players and owners, the ones who are capitalizing on the profits of the new publicly funded stadium, spending their earnings in the surrounding economy.

Civil Rights of 1972, Title IX

The Education Amendments Act of 1972, otherwise known as Title IX, was arguably the most influential Civil Rights law passed. The legislation states, “No person in the United States shall, on the basis of sex, be excluded from participation in, be denied the benefits of, or be subjected to discrimination under any education program or activity receiving federal financial assistance,” Title IX (36). It was not until 1987 that the Civil Rights Restoration Act formally incorporated athletics to be under the scope of Title IX (37).

Title IX is admired for the immense influence it has had on female participation in sports since its adoption. When the law was passed, “Title IX produced an 875% increase of female participation in high school sports and a 435% increase in intercollegiate athletics” (37). Between 1972 and 2012, there was an increase of 52,000 female participants at the intercollegiate level (37). The opportunity for equal participation among males and females has slowly realized over the past 50 years. While Title IX was a landmark decision when it was signed into action, the Act’s evolution has had resounding success.

Thesis

There is a prevalent issue with the lack of ethnic diversity among NFL ownership, and with the amount of authority that current owners possess, there is a need for progressive reform. The NFL has ample room for change under a new ownership structure, adapting to today’s needs but also anticipating future challenges that may lie ahead.

Research Methods

This manuscript used a mixed methods approach to conduct the research leading to recommended proposals and a conclusion on the subject matter. A combination of observation, secondary data analysis/archival study, and personal interview was used. As for the interview subjects, the process of selecting and contacting each interviewee was based off of their professional experience in day-to-day executive sport management, law, and sport franchise ownership.

Although the information was gleaned from interviews with a few industry executives, several qualified individuals declined to comment due to the sensitivity of the subject matter. The individuals who declined to comment were senior-level executives from the NFL league office, NFL Players Association, Morgan Stanley Wealth Management, Washington Commanders, U.S. State Department, and the MLS’s D.C. United.

Recommended Proposals

While each proposal has the aptitude to stand on its own, the implementation of enacting all of them together will yield greater results.

Rooney Rule

The Rooney Rule is purely a placeholder because the NFL has deep-rooted racial prejudices in the ownership box, and nobody is willing to question the current and long-standing owners’ values. The National Action Network Founder and President, Rev. Al Sharpton, recently stated that the Rooney Rule is nothing more than the owners deceptively seeking actual diversity (38). If white men are continuously making all of the decisions for the league, diversity and inclusion will not reach their full potential. In turn, the league will suppress itself from success. “The change has to be more sustainable; we have to go to the core of the issue… respect is still the overarching theme of being kind in humanity,” (39). The goal is to reduce unconscious bias and create inclusion.

Instead of making repetitive adjustments to the Rooney Rule as it is now and never producing notable progress, the change needs to come from within the 32 ownership groups. Frank Dobbin and Alexandra Kalev confirmed that organizations doubling down on their programs to increase diversity often make things worse (40). Once greater diversity is seen across the ownership ranks, a significant difference can occur for the league. If a person of minority status is an owner of a franchise, applying the Rooney Rule should, in theory, no longer be necessary. Jim Rooney, son of Dan Rooney, the longtime owner of the Pittsburg Steelers and whom the Rooney Rule was named, stated, “We look at the workplace in general if we are pushed to make a decision, that otherization that plays out within ourselves, we are going to hire someone that looks like us, feels like us, and makes us feel comfortable,” (41).

A Rooney Rule would be difficult to justify and legally uphold if applied to general partners. On the flip side however, limited partner ownership must be within the scope of the Rooney Rule. If a general partner is searching for a limited partner to own a percentage of the franchise, a candidate of minority status is the only option. Although many limited partners only have passive roles within an organization, the appearance and representation of a diverse owner can speak volumes about a progressing culture. Not only will the presence of a person of color be felt among the rest of the franchise, the majority owner now has the potential to see the realized gains of incorporating new perspectives. Michael Huyghue, a longtime lawyer, NFL front office executive, and consultant to the NFL Commissioner, acknowledged that the NFL currently does not have a Rooney Rule for owners, however, he was captivated by the concept. “Diverse ownership needs to be viewed as diverse leadership” (39). Diverse leadership creates a widely successful advantage.

In the case of a limited partner being outside of the immediate family of the general partner, the NFL needs to implement that there is at least one person of minority status be involved in the ownership group. The mandate would serve to merge differing opinions and divest the equity to external individuals not related to the general partner. “Diversity enriches the game and creates a more effective, quality organization from top to bottom” (6).

Although the Denver Broncos were recently sold to Rob Walton and his daughter Carrie Walton-Penner, both white individuals, there is progress within the ownership group. Walton’s consortium that purchased the team includes former United States Secretary of State Condoleezza Rice, Ariel Investments CEO and President Mellody Hobson, and Formula 1 Champion Sir Lewis Hamilton (42). With all three of these individuals being of diverse ethnic backgrounds, it helps the Walton ownership group pave a new way forward. Soon after Rice, Hobson, and Hamilton were announced as limited partners, Walton said, “We think diversity is important. We think diverse organizations are more successful organizations” (42).

NFL Board of Directors

There is a lack of clarity with the newly proposed Diversity Advisory Committee. First off, there should be more than one committee. In order to increase oversight and to have the ability to enact change across the league, there need to be three additional committees providing adequate time and resources. Essentially, two committees would be tasked with overseeing the American Football Conference (AFC) and two with overseeing the National Football Conference (NFC). Secondly, the committees should have the ability to suspend or punish an owner or franchise for failing to incorporate operational initiatives. Since these committees were hand-selected by the league itself, they have the authority to provide appropriate disciplinary action when needed. Operating as a non-bias, independent board of directors, these committees will provide checks and balances to every franchise and ownership group based on ethical hiring practices, emphasizing equitable opportunity.

Private Equity

Private equity funds have allowed sports leagues and franchises to grow and operate in different ways than ever before. If the NFL were to add institutional investment funds to its ownership group, it would allow for more profitable and viable growth to occur. Through private equity, turnover in ownership, particularly at the limited partner level, would transpire much more frequently. Adding additional consortiums to the mix, whether single individuals, groups, or institutional funds, creates a theoretical end date for a limited partner’s investment. Although if not an end date, at least a period of which they have the opportunity to liquefy the asset and cash out on their portion of equity. Jez Moxey, a longtime English Premier League executive who specializes in mergers and acquisitions, expects the NFL to follow suit with its counterparts and relax its own rules to accommodate private equity. “From a business and rising valuations standpoint, private equity will come into play for the NFL, as there does not seem to be any other option” (43). Meanwhile, as the NFL continues to watch the NBA, NHL, MLB, and MLS engage with private equity groups, its franchise valuations are steadily rising with inadequate control. Implementing venture capital into its franchise consortiums provides a logical solution.

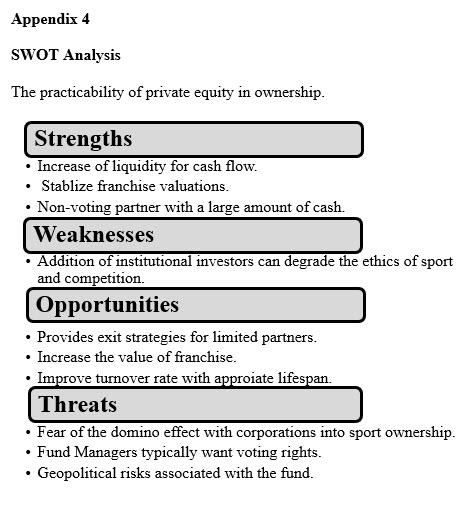

Furthermore, by referencing the NBA, and the influx of liquidized cash acquired through private equity, franchises now have additional funds for facility improvements and other ventures. Due to the rarity of NFL ownership turnover, cash flow from new partners does not exist (see Appendix 4 for SWOT analysis on the practicality of private equity in NFL ownership consortiums).

Publicly Funded Stadium

While the debate of public vs. private funding for facility improvements will likely continue for decades without a clear solution, measures can be taken to reduce the effects of municipalities taking the burden. If an NFL franchise is looking to build or renovate a stadium financed by publicly funded tax-payer money, one of the ways to stimulate diversity is by examining an example set by former Atlanta city Mayor Maynard Jackson. In 1974, Mayor Jackson gave an ultimatum to the city of Atlanta and Fulton County business officials that at least 25% of the construction contracts for the expansion of Hartsfield Atlanta International Airport be set aside for minority-owned firms or businesses (44). Jackson went to the extreme, stating, “we simply won’t build the airport if you don’t agree to this” (44). After final negotiations, 20% of the contracts were awarded to minority-owned businesses leading to a significant stimulus of economic activity across the minority community (44). The result of Jackson’s ultimatum gave way to a stronger minority middle class and further endorsed minority-led businesses for public works projects in the coming years. Following Mayor Jackson’s death in 2003, the Hartsfield Atlanta International Airport was renamed Hartsfield-Jackson Atlanta International Airport to honor his legacy (45).

This same proposition can be given to NFL franchises and their owners. When conducting business, the NFL has continuously operated with a carrot and stick approach (46). Instead of allowing the NFL to perpetually exploit public subsidies, the government must implement a similar policy to the late Mayor Jackson’s. If a franchise requests a government subsidy to finance facility improvements, the franchise must grant a proportion of the construction contracts (e.g., 25-30%) to minority-led businesses. If the franchise does not agree with the terms, the organization must find an alternative method to fund such projects.

According to Wilkins, stadiums have increasingly been relocated and constructed in low-income, black neighborhoods, resulting in the displacement of that community (47). Due to the low property value of such land, the franchise more often than not deems that it can replenish the appeal of the respective neighborhood. Essentially, NFL franchises and their selection of stadium locations in low-income neighborhoods are fueling gentrification, directly distressing people of color. Awarding the contracts associated with stadium improvements to minority-led businesses will lessen the hardship of the displaced communities.

Fiscal Considerations

Since the NFL does not allow corporate businesses or institutional investors into its ranks, it needs to modify the NFL bylaws to incorporate private equity funds. A private equity firm would take place as a limited partner with no voting rights. Based on the NBA’s model of integrating private equity at the ownership level, the NFL needs a similar set of guidelines that pertain to its structure.

- An equity group cannot own more than 10% of a single franchise.

- No franchise can collectively have more than 25% of its ownership group comprised of private equity investors.

These two requirements would allow additional liquidity at the ownership level without diminishing the franchise’s brand value. Similar to the NBA, NHL, MLB, and MLS, the NFL league and its 32 owners will need to preapprove each firm interested in bidding for a limited stake. The main criteria are excellent financial records and superior ethical standards. For example, the Miami Dolphins are worth an estimated $4.06 billion, slightly above the average NFL valuation (24). If a private equity firm is interested in purchasing a 10% stake in the Dolphins, it would cost roughly $460 million. Then, if the Dolphins had multiple private equity firms invested in the franchise, no more than $1.15 billion of its estimate could be associated with institutional firms. The capital collected from institutional investors offers the franchise liquid cash for facility and stadium improvement projects.

Recently, the highest-recorded publicly funded stadium built was Allegiant Stadium, home of the Las Vegas Raiders. The stadium was completed in 2021 and used an estimated $750 million in public funds which accounted for approximately 42% of the overall cost. The remaining costs were paid for by loans and private funds, totaling $1.8 billion (48). Even after a stadium project is completed, the public is stuck with the bill for years. The residents of Chicago, as of 2019, are still paying off a $137 million debt on the White Sox ballpark even though the stadium was completed in 1991 (48). The Buffalo Bills are set to surpass the Raiders and utilize $850 million of public subsidies on the tender. Totaling $1.4 billion, the Pegula family has been approved for roughly 61% of the stadium to be financed via state and local taxpayers. Erie County, where the stadium will be located, is expected to cover $200 million, while the state of New York will finance $600 million (49).

As owners accumulate wealth from their own NFL franchise and other business ventures, facility improvements should be on their account. If the franchise turns to the government for subsidy support, a proportion (25-30%) of the contracts must be awarded to minority-led businesses. For example, between the proposed Bill’s stadium financing projections and if deploying 30% of the contracts to minority-led companies, $340 million worth of business would be inserted into the displaced community. This initiative will help drive sustainable results for minority employers in the short and long term.

Measurement of Success

A measurement of success that can be directly traced to the recommendations is ownership turnover. The general public will typically only find out about the general partner transitioning ownership or selling the franchise when there is ownership turnover. Rarely will the general public hear about limited partners and their ownership transactions due to the lack of public record of their involvement with a particular club. Increasing the turnover rate, whether at the general partner level or limited partner level, will result in more change, and alternate forms of leadership will ensue.

Another measurement of success can be found in the TIDES Report. The TIDES Diversity and Inclusion report is published on an annual basis and will have quantitative statistics concerning the diversity of the NFL. Transformations involving diversity and inclusion do not happen overnight, especially when working with an entity as big as the NFL. Even though it has been over 50 years since Title IX was enacted, the effects of the Civil Rights Act are still being discovered today (37). The NFL is set to embark on a journey similar to Title IX. The TIDES report will detail every diverse individual in a leadership position across the league, shining a light on the progress emerging across the league.

Negotiating with governmental politicians on publicly funded stadiums and how to improve the communities that are impacted by gentrification is an additional measurement of success. The late Mayor Jackson provided a precedent for public subsidies and how to utilize them to benefit all stakeholders. While social reform rarely originates directly from the source, this proposal is to provide a change in the local community instead of applying it to the franchises and owners themselves.

The 32 owners hold the keys to the league’s destiny. The recommendations can only come to fruition if the current owners enact reform.

CONCLUSIONS

The NFL and its owners have always operated full well, knowing they have a convincing influence over society. Through various instances, the NFL has gradually demonstrated its willingness to modernize. Applying the Rooney Rule to limited partners, introducing private equity into franchise ownership consortiums, and modifying governmental agreements for public subsidies will advance opportunities for diversity and change. Similar to the Civil Rights Act of 1972 and Title IX, implementing a transformation of this magnitude to an enterprise such as the NFL does not occur overnight. The NFL can be a catalyst for change, and by taking the initiative, a revolution has the freedom to transpire. The only way to realize such changes is to have the 32 owners agree to equitable opportunity. Without the endorsement from the owners, prejudice will remain the status quo.

APPLICATIONS IN SPORT

In accordance with the National Football League bylaws, the above proposals act as a road map for broadening the franchise ownership pool. While this manuscript was written with the intent of the National Football League, the recommended proposals have the ability to be adjusted for any of the major professional sports leagues in the United States.

DEDICATION

This manuscript is dedicated to my Mom and Dad. Endless love, support, and encouragement

REFERENCES

1. Smith, T. (1988). Outside the Pale: The Exclusion of Blacks from the National Football League, 1933 -1946. Journal of Sport History, 15(3), 255-281.

2. Black history and American professional football, a story. African American Registry. (2022, November 14). Retrieved from https://aaregistry.org/story/black-contributions-to-american-professional-football-are-many/#:~:text=Several%20NFL%20teams%20stood%20out,signing%20Bobby%20Mitchell%20in%201962.

3. Coates, T. (2011). A History of Segregation in the NFL. The Atlantic. Retrieved from https://www.theatlantic.com/entertainment/archive/2011/11/a-history-of-segregation-in-the-nfl/248625/.

4. Eagly, A. H., & Chin, J. L. (2010). Diversity and Leadership in a Changing World. American Psychologist, 65(3), 216–224. https://doi.org/10.1037/a0018957

5. Lambert, J. (2016). Cultural Diversity as a Mechanism for Innovation: Workplace Diversity and the Absorptive Capacity Framework. Journal of Organizational Culture, Communications and Conflict, 20(1), 68-77. Retrieved from https://www.proquest.com/scholarly-journals/cultural-diversity-as-mechanism-innovation/docview/1804899646/se-2?accountid=11091

6. NFL Operations. (n.d.). The Rooney Rule. NFL Operations. Retrieved from https://operations.nfl.com/inside-football-ops/diversity-inclusion/the-rooney-rule/

7. Archie, A. (2022, March 29). The NFL requires teams to hire women or minorities as coaches for the 2022 season. NPR. Retrieved from https://www.npr.org/2022/03/29/1089386609/nfl-diversity-dei-women-minorities-owners-meeting-coaches

8. Ebrahimji, A. (2022, March 29). The NFL says teams must hire a minority or female offensive coach. CNN. Retrieved from https://www.cnn.com/2022/03/29/sport/nfl-minority-women-coaches-rooney-rule

9. Seifert, K. (2022, March 28). NFL says all teams must add minority offensive coach, expands Rooney Rule to include women. ESPN. Retrieved from https://www.espn.com/nfl/story/_/id/33617341/nfl-says-all-teams-add-minority-offensive-coach-expands-rooney-rule-include-women

10. Burton, L. J., Kane, G. M., & Borland, J. F. (2015). Sport leadership in the 21st century. Jones & Bartlett Learning.

11. Constitution and Bylaws – NFL. NFL Constitution and Bylaws. (1970, February 1). Retrieved from https://www.onlabor.org/wp-content/uploads/2017/04/co_.pdf

12. Soshnick, S. and Novy-Williams, E., 2022. Jeter Sells Out of Marlins / Broncos Sale Handcuffs NFL. Sporticast: The Business of Sports.

13. Greenberg, M. J. (2019, January 22). NFL cross-ownership rule changes: Sports Business: Martin J. Greenberg. Greenberg Law Office. Retrieved from https://www.greenberglawoffice.com/nfl-cross-ownership-rule-changes/

14. Sullivan, P. (2018, February 2). How to bid for the N.F.L.’s biggest prize: Team ownership. The New York Times. Retrieved from https://www.nytimes.com/2018/02/02/your-money/buy-nfl-team.html

15. Novy-Williams, E. (2020, October 29). NFL preparing for owners to restructure as election, possible tax changes loom. Sportico.com. Retrieved from https://www.sportico.com/leagues/football/2020/nfl-owners-tax-memo-election-1234615743/

16. Lapchick, D. (2021). The 2021 Racial and Gender Report Card: National Football League. Orlando: The University of Central Florida.

17. Leeds, M. A., Allmen, P. V., & Matheson, V. A. (2018). The Economics of Sports (6th ed.). New York, NY: Routledge, Taylor & Francis Group

18. Newton, D. (2017, December 18). Carolina Panthers owner Jerry Richardson, 81, selling team. ESPN. Retrieved from https://www.espn.com/nfl/story/_/id/21798557/carolina-panthers-owner-jerry-richardson-selling-nfl-team

19. Belson, K. (2018, May 15). Carolina Panthers will be sold for $2.2 billion to David Tepper. New York Times. Retrieved from https://www.nytimes.com/2018/05/15/sports/football/carolina-panthers-sold-jerry-richardson-david-tepper.html

20. Heath, J. (2022, March 7). NFL has a new stipulation for parties who want to bid for Broncos. USA Today. Retrieved from https://broncoswire.usatoday.com/2022/03/07/denver-broncos-ownership-update-nfl-new-stipulation/

21. Gabriel, P. (2022, August 9). NFL approves sale of Broncos, making Rob Walton League’s wealthiest owner. USA Today. Retrieved from https://www.usatoday.com/story/sports/nfl/broncos/2022/08/09/denver-broncos-sale-approved-rob-walton-penner-walmart/10271281002/

22. Legwold, J. (2022, August 9). NFL owners unanimously approve $4.65 billion sale of Denver Broncos to Walton-Penner Group. ESPN. Retrieved from https://www.espn.com/nfl/story/_/id/34374799/nfl-owners-unanimously-approve-sale-denver-broncos

23. Ozanian, M. (2018, March 30). Increase in NFL debt limit will help sale of Carolina Panthers. Forbes. Retrieved from https://www.forbes.com/sites/mikeozanian/2018/03/30/increase-in-nfl-debt-limit-will-help-sale-of-carolina-panthers/?sh=d6afc2edb672

24. Badenhausen, K. (2022, September 17). Dallas cowboys lead Sportico’s 2022 NFL valuations at $6.9 billion. Sportico. Retrieved from https://www.sportico.com/valuations/teams/2022/dallas-cowboys-lead-sporticos-2022-nfl-valuations-at-6-9-billion-1234638658/

25. Stone, L. (2021, December 9). Jody Allen reportedly is ‘not happy’ with the Seahawks’ struggles. how will she address them? The Seattle Times. Retrieved from https://www.seattletimes.com/sports/seahawks/jody-allen-reportedly-is-not-happy-with-the-seahawks-struggles-how-will-she-address-them/

26. Klein, G., Morgan, E., & Miller, J. (2020, July 17). 3,449,990,800% return on investment? welcome to the NFL owners club. Los Angeles Times. Retrieved from https://www.latimes.com/sports/story/2020-07-17/nfl-billionaire-team-owners-who-rule-sports-united-states

27. Mai, H. J. (2021, March 19). New $113 billion NFL media rights deal gives fans more options to watch games. NPR. Retrieved from https://www.npr.org/2021/03/19/979178471/new-113-billion-nfl-media-rights-deal-gives-fans-more-options-to-watch-games

28. Killingstad, L. (2021, July 19). Why private equity investors love the NBA. Front Office Sports. Retrieved from https://frontofficesports.com/why-private-equity-investors-love-the-nba/

29. Pompliano, J. (2021, March 26). Professional sports teams continue to increase in value. Professional Sports Teams Continue to Increase in Value. Retrieved from https://huddleup.substack.com/p/professional-sports-teams-continue?s=r

30. Browndorf, C. (2021, May 21). A New Kind of Pitch: The Rise of Sports Dedicated Private Equity Funds and the Future of the Single Entity Defense, 28 Jeffery S. Moorad. Sports L.J. 335. Retrieved from https://digital.commons.law.villanova.edu/msl.j/vol28/iss2/3

31. Mike Davey (2022) Personal Communication.

32. Kerr, J. (2022, March 28). Bills announce $1.4 billion, open-air stadium in Orchard Park, set to be completed in 2026. CBSSports.com. Retrieved from https://www.cbssports.com/nfl/news/bills-announce-1-4-billion-open-air-stadium-in-orchard-park-set-to-be-completed-in-2026/

33. Noll, R. G., & Zimbalist, A. S. (1997). Sports, jobs, and taxes: The economic impact of sports teams and stadiums. Brookings Institution Press.

34. Drukker, A. J., Gayer, T., & Gold, A. K. (2020). Tax-exempt municipal bonds and the financing of professional sports stadiums. National Tax Journal, 73(1), 157–196. https://doi.org/10.17310/ntj.2020.1.05

35. Rosen, D. (2013, March 1). Socialize costs, privatize profits. CounterPunch.org. Retrieved from https://www.counterpunch.org/2013/03/01/socialize-costs-privatize-profits/

36. Education Amendments Act of 1972, 20 U.S.C. §§1681 – 1688 (1972)

37. Belkoff, C. (2020). The impact of Title IX on women in intercollegiate sports administration and coaching. The Entertainment and Sports Lawyer, 36(3), 45-59. https://www-proquest-com.proxy.library.georgetown.edu/trade-journals/impact-title-ix-on-women-intercollegiate-sports/docview/2584599318/se-2?accountid=11091

38. Pickman, B. (2022, February 8). Civil rights leaders call on NFL to replace Rooney Rule. Sports Illustrated. Retrieved from https://www.si.com/nfl/2022/02/08/civil-rights-leaders-rooney-rule-replacement-meeting

39. Micheal Huyghue (2022) Personal Communication.

40. Dobbin, F., & Kalev, A. (2016, July). Why Diversity Programs Fail. Harvard Business Review. Harvard Business Review. Retrieved from https://hbr.org/2016/07/why-diversity-programs-fail.

41. Barbaro, M., 2022. The Rule at the Center of the N.F.L. Discrimination Lawsuit. The Daily.

42. Gorman, T. (2022, August 10). The Denver Broncos have new owners – officially – after NFL owners give final OK. Colorado Public Radio. Retrieved from https://www.cpr.org/2022/08/09/the-denver-broncos-have-new-owners-officially-after-nfl-owners-give-final-ok/

43. Jez Moxey (2022) Personal Communication

44. Dingle, D. T. (2009, February 10). Maynard Jackson: The Ultimate Champion for Black Business. Black Enterprise. Retrieved from https://www.blackenterprise.com/maynard-jackson-the-ultimate-champion-for-black business/

45. Pritchett, A. R. (2021). Hartsfield-Jackson Atlanta International Airport. In New Georgia Encyclopedia. Retrieved from https://www.georgiaencyclopedia.org/articles/business-economy/hartsfield-jackson-atlanta-international-airport/

46. Scott Burrell (2022) Personal Communication

47. Wilkins, D. (2016) “The Effect of Athletic Stadiums on Communities, with a Focus on Housing.” Clark University. International Development, Community and Environment (IDCE). 88. https://commons.clarku.edu/idce_masters_papers/88

48. Sharp, R. (2019, May 22). How was your stadium, arena or ballpark funded? Global Sport Matters. Retrieved from https://globalsportmatters.com/business/2019/05/22/who-paid-for-your-stadium/

49. Ferré-Sadurní, L. (2022, March 28). Buffalo Bills strike deal for taxpayer-funded $1.4 Billion stadium. The New York Times. Retrieved from https://www.nytimes.com/2022/03/28/nyregion/buffalo-bills-stadium-deal.html

Appendix

Appendix 1

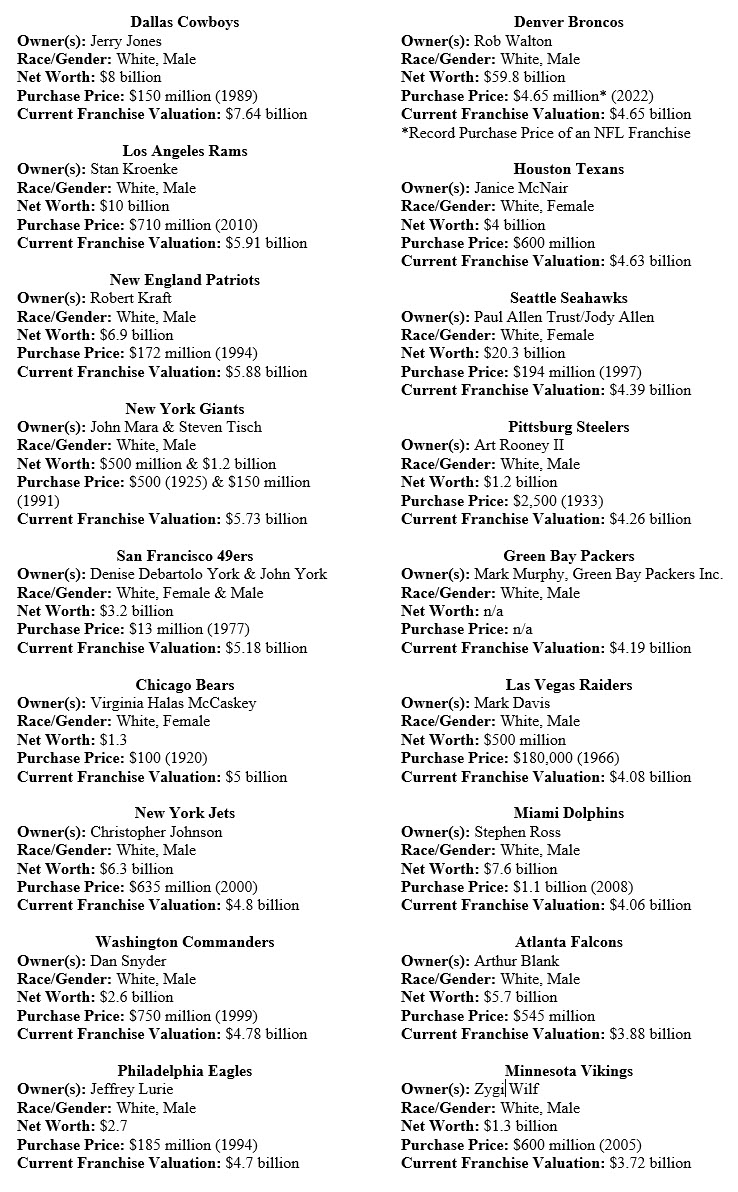

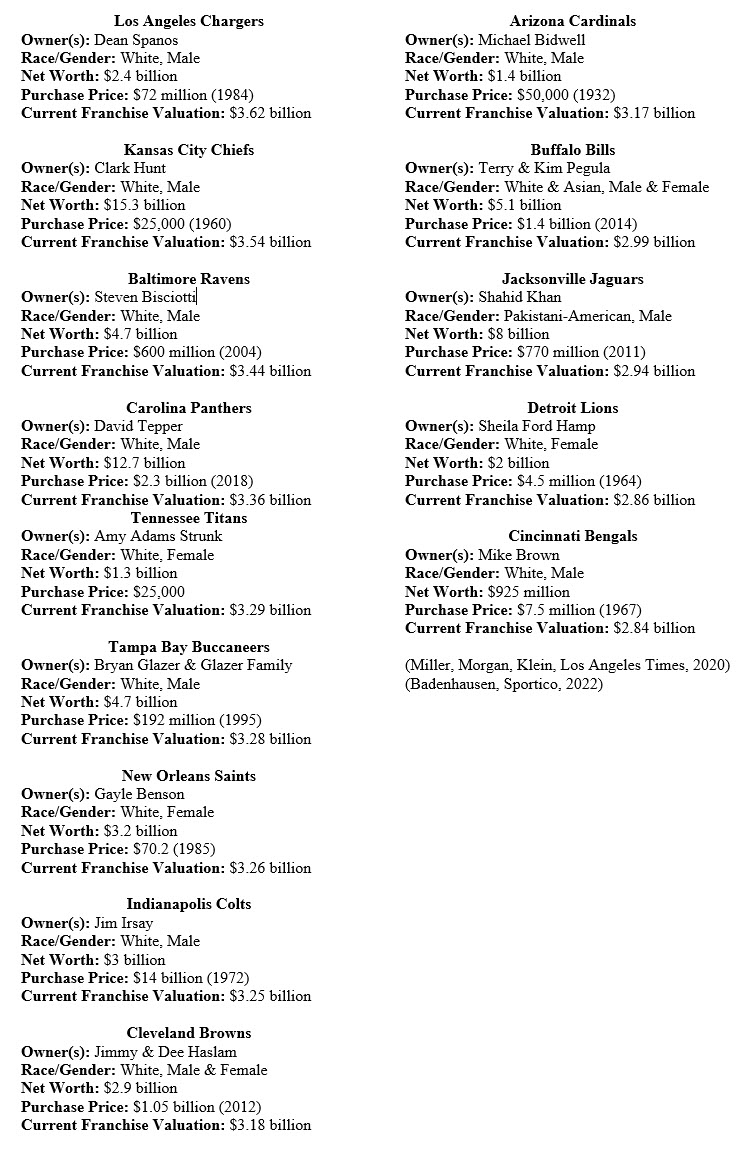

List of the 32 franchises, the general partner(s), the net worth of the general partner, the purchase price of the franchise, and the current valuation. The franchises are listed in order from most valuable to less valuable. References: LA Times – Owner Net Worth and Purchase Price (25). Sportico – Current Franchise Valuations (23).

Appendix 2

NFL Diversity Advisory Committee

Pamela Carlton, Founder, and President, Springboard

Peter Harvey, Former Attorney General of New Jersey; Partner, Patterson Belknap

Patricia Brown Holmes, Managing Partner, Riley Safer Holmes & Cancila

Stefanie K Johnson, Associate Professor, University of Colorado Boulder Leeds School of Business

Rick Smith, Former General Manager, Houston Texans

Don Thompson, CEO and Founder, Cleveland Avenue, LLC, and Former President and CEO of McDonald’s Corporation

(NFL Operations, 2022)

Appendix 3

NFL Workplace Diversity Committee:

Art Rooney II – Pittsburg Steelers (Chair)

Michael Bidwell – Arizona Cardinals

Arthur Blank – Atlanta Falcons

Javier Loya – Houston Texans

John Mara – New York Giants

George McCaskey – Chicago Bears

Ozzie Newsome – Baltimore Ravens

Kim Pegula – Buffalo Bills

(TIDES, 2021)

Appendix 5

Interviewees

Mike Davey – Mike Davey is a limited partner of a Serie A Italian football club. Prior to joining professional sports ownership, Davey was Head of Securities Trading Floor at Brown Advisories.

Michael Huyghue – President of Michael Huyghue & Associates LLC. When examining race and professional sports, Mr. Huyghue is a pioneer, explicitly looking at NFL front offices. Widely known as the youngest and first black general manager in the NFL, Huyghue took his career to the NFLPA, NFL Management Council, Jacksonville Jaguars, and served as the Commissioner of the United Football League. Most recently, Huyghue has aided as a consultant to the NFL Commissioner and its 32 owners on the matters of minority hiring and social justice.

Jez Moxey – Moxey is a long-time executive in the English football industry, previously been the Chief Executive Officer of the Wolverhampton Wolves, Norwich City, Stoke City, and currently at Burton Albion. As a pivotal board member of General Sports Worldwide, Moxey provides strategic team mergers and acquisitions expertise.

Scott Burrell – Burrell is Senior Council at Leftwich LLC., a law and consultancy firm in Washington, D.C., specializing in government operations and business. Through various instances, Burrell has negotiated and conducted successful transactions involving district officials and business entities. Burrell is a faculty member at Georgetown University, teaching Sports Law.