This paper bridges a theoretical gap between early celebrity endorsement and hero worship literature. Additionally, the model connects a successful, winning athlete with several established branding constructs. The Roethlisberger Effect takes early theory proposed over 35 years ago in “The Namath Effect” and applies it with a modern touch. Given that the NFL is often referred to as a “copycat league” – i.e. when something works, all other teams work quickly to replicate it – the impact that Roethlisberger has had upon other league and team management philosophies is rather profound.

This paper is an updated version of a poster presentation I authored for the 7th Sport Marketing Association (SMA) Conference (2009).

There are three parties involved in a simple sponsorship mechanism: the sponsor, the sponsored event or team, and the consumers (fans). However, this structure becomes more complicated in some cases where sub-sponsors exist such as in international sporting events. In these cases, would an overarching event influence sub-sponsorship such as team sponsorship? Based on this question, this study aims to investigate the influence of overarching brand on team sponsorship effect, along with consumers’ attitudes toward team sponsors, team identification, and patriotism.

This study was conducted in the context of the 2010 World Cup with the United States team as a target subject. A total of 455 usable surveys were collected from the students at a Division I university two weeks prior to the 2010 World Cup. The results of multiple regression showed that only identification with the US National team (β= .54) and attitude toward the sponsoring companies (β= .28) were significant predictors (F(4,450) = 128.43, p < .00, R2=.53), explaining 53 percent of intention to purchase sponsors’ product. Interestingly, the attitude toward the World Cup and patriotism were not influencing factors on respondents’ intention to purchase sponsors’ products. (more…)

Submitted by Timothy Baghurst, Earl Murray Jr., Chris Jayne and Danon Carter

ABSTRACT

The current and future funding condition for junior college (JC) athletics is unclear, and an athletic program’s budget and funding is usually the responsibility of the athletic director. The purpose of this qualitative phenomenological study was to explore the lived experiences and perceptions of junior college athletic directors to understand financial and leadership issues associated with athletic programs. Sixteen athletic directors (12 male, 4 female) from the same athletic conference in the state of California were interviewed and asked 17 open-ended questions about leadership and the financial issues associated with junior college athletic programs. Three primary themes emerged including leadership, roles and responsibilities, and an unexpected third theme of the student-athlete. Findings and their application to athletic director administration are discussed.

INTRODUCTION

College athletics have become big business, and a university athletic director (AD) plays an integral role in the success of the athletic programs. Colleges and universities at all levels require the managerial skills of an AD. Although leadership and administration of athletics is a frequent focus of research at the National Collegiate Athletics Association (NCAA) level, community college (hereto forth referred to as junior college; JC) programs have received little attention. For example, NCAA Division I athletic budgets may vary widely, but substantial budgets are common (14). Thus, application of findings at this level to JC athletic programs is difficult, as JC ADs may face more responsibilities in addition to fewer funding sources and athletic staff at their disposal. Therefore, the focus of this qualitative phenomenological study was to explore the lived experiences of JC ADs in order to determine how they use their leadership to overcome financial challenges experienced by their athletic programs.

Qualities of an AD

Robertson (2008) highlights several traits and skills necessary to be a successful AD. First, he or she must have the capability of creating an environment that helps all members of the program flourish, and all members of the athletic program must have the same goal in mind. Second, an AD must exhibit the ability to take risk, solve problems, think critically, and be a decision maker. Third, they must have the fiscal savvy to promote their university/college in a way that draws fan and community support thereby generating revenue. Thus, fiscal responsibilities of athletic programs are one of the most important challenges athletic administrators deal with at all levels (20).

JC Leadership Qualities

Nahavandi (2006) defined a leader as “any person who influences individuals and groups within an organization, helps them in the establishment of goals and guides them toward achievement of those goals, thereby allowing them to be effective” (p. 4). Another definition of leadership is “the capacity to influence others by unleashing their power and potential to impact the greater good” (4). Consistent with both definitions, leadership requires the ability to influence followers and guide them toward a goal.

Athletic directors are expected to display leadership skills in overseeing the day-to-day operations of the athletic department, but leadership is also necessary to manage the budget and financials of the program (13). There are several qualities of effective leadership as well as factors that impact the effectiveness of leadership. Effective leadership is defined by the effect on followers. Key traits of effective leaders as described by Kirkpatrick and Locke (1991) include drive, integrity, intelligence, motivation to lead, and knowledge of the business. Overall, leadership success is defined by the effectiveness of leaders to influence followers in every relevant aspect.

Junior college ADs must possess certain leadership qualities or characteristics to be successful. These characteristics include ethics or strong moral values, competence, self-confidence, and a desire to influence (28). Followers must trust the decisions and behaviors of ADs as well as believe in the direction being led. Leadership styles most attributed to ADs are transformational and situational leadership, as these styles incorporates change management, practicality, and flexibility as well as the success these leadership styles have on influencing others.

JC Athletic Finances

The funding for state colleges are being reduced across the country; and this is causing economic instability within many JC athletic programs (34). Junior college ADs are faced with difficult decisions when it comes to their athletic programs, which primarily revolve around the sustainability of the program. In many cases, there is outside pressure to add athletic teams to their program, while in others situations, ADs have to decide to keep a team or cut it from their program to save money (36). In 2009, Mississippi Governor Haley Barbour addressed the state’s JC ADs to explain that they needed to scale back the number of athletic teams that they offered, or the schools would have to drop athletics altogether (34).

Leadership is a key to any successful company, and sports administration is no different. However, how an AD may use his or her acquired leadership techniques to maintain and allow an athletic department to flourish under his or her guidance is unclear. This is particularly true at the JC level, where research is limited. Although there are similarities between the roles and responsibilities of ADs at JC compared with larger four-year universities, there are also differences. According to Lewis & Quarterman (2006), the three most important decisions and choices ADs make for managing and leading JC athletic programs are the enjoyment of athletics, the athletic environment, and a desire to learn more about the sports business. ADs from large universities have a greater focus on fiscal management where much of their time is focused on management, leadership, finance, marketing, ethics, legalities, and governance (2). This is not to say that JC ADs ignore ethical or legal issues, for example, but it is not considered their priority.

Although there are large financial deviations within NCAA Division I athletic programs, (14; 37), only a few operate profitably (10). Thus, the university is placed with a financial burden of justifying the existence of a program, and many DI ADs must turn to donors to gain the fiscal capital needed to balance their athletic budgets (35). For example, in the summer of 2012, facing a $4 million deficit, Maryland University decided to eliminate seven competitive athletic teams (17). Similarly, other prominent universities have taken drastic measures to ensure the survival of their athletic programs as a whole: University of California-Berkley had to cut five teams in 2010 and Rutgers University was forced to drop six competitive athletic teams in 2007 (3).

Unfortunately for ADs at the JC level, the financial situation is even bleaker. Most junior colleges lack the same opportunities. Fewer boosters are available and revenue generated at events is lower. Sustainability is a larger concern because of many educational cuts in state funding (Steinback, 2010). Success at the National Junior College Athletic Association (NJCAA) level does not always equal financial gain or even a program the next year. For example, in 2009 Minneapolis Community and Technical College lost only its second game of the year in the NJCAA DIII national championship game only to have the athletic department shut down completely shortly after. In order to continue to have an athletic program, some institutions have been required to cut the football program; although it is the biggest revenue provider, it is also the most expensive (34).

Study Purpose

The roles and responsibilities of an NCAA AD are well-documented, but less so are those of a JC AD, particularly as they pertain to leadership and financial skills. The current and future funding condition for JC athletics is unclear (6). A better understanding of the skills and qualities necessary for success could be vital as JCs search for their next AD. Therefore, the purpose of this study was to explore the perceived leadership and financial skills of 16 JC ADs to better understand how leadership and financial skills in athletic programs might contribute to success. The qualitative, phenomenological study consisted of semi-structured interviews and asked ADs not only what it was like to serve in that capacity, but also to explain, (1) the relationship between ADs’ perceptions about leadership and funding JC athletic programs, and (2) the relationship between ADs’ perceived leadership skills and financing JC athletic programs. It was intended that ADs explain in general how they perceive leadership and how it is relevant in managing programs. Then, participants were asked to detail their perceived leadership skills to manage programs effectively.

METHOD

Participants

Participants were 16 ADs (12 male, 4 female) from JCs in California who were purposefully selected because they were knowledgeable about athletic programs and financing (11). Participants’ experience ranged between 10 and 21 years (see Table 1). Currently employed ADs were used to provide real-time feedback as opposed to retroactive data.

Procedures

Following university IRB approval, 20 ADs currently employed at a JC within the same athletic conference were mailed a letter to request an interview. From the 20 requests, three participants returned the letter agreeing to participate. The remaining 17 participants were contacted by telephone from which a further 13 agreed to participate.

Prior to each interview participants were asked to sign a consent form. All face-to- face interviews lasted between 25 and 50 minutes and were conducted within a one-month period. The interviews were conducted at a neutral site of the participant’s choosing. A mini cassette recorder was used to record all interviews in their entirety. All interviews were manually transcribed by the researcher using audacity-recording software. Following transcription, each participant was sent his or her transcript to confirm its accuracy.

Instruments

In qualitative research, the researcher is the primary instrument by exploring the phenomenon under study (7). Open-ended questions navigate and focus descriptions of a particular experience through intuition and reflection of that experience. A phenomenological study requires the interviewer to achieve, or attempt to achieve, a state of epoche, the elimination of suppositions and placement of knowledge above every possible doubt (24). Thus, the primary researcher made every effort to suppress any predisposed opinions or presumptions during this study regarding the phenomenon. This allowed the researcher to grasp and freshly comprehend the participants’ experiences with the phenomenon (12).

A face-to-face interview technique with open-ended questions was the most appropriate data collection method as it allowed for some deviation while simultaneously ensuring consistent structure across interviews (12). The semi-structured, open-ended questioning interview process was designed to direct the participant toward his or her lived experiences (27).

NVivo9™ software, in accordance with the modified van Kaam data analysis method, was used to analyze interview transcripts, and identify common themes, and patterns (25). Furthermore, the software package provided a digital transcript of audio files, import, and coding of interview transcripts and aided the exploration of potential emerging themes using a step-by-step process.

Data Validity, Reliability, and Triangulation

Validity is how accurately the account represents participants’ realities of the phenomenon and their credibility (16). To establish the validity for this study, transcripts were shared with the participants to ensure that the data was accurate prior to analysis, which is an important dimension of good quality research (9). This allowed participant to edit, revise, or add information prior to data analysis, none of which did. If both validity and reliability are the goal of qualitative research, the use of triangulation to record the construction of reality is appropriate (18). Triangulation occurs when different data sources, methods of data collection, or types of data are evidence to support research data (12). In the present study, participants were sent interview transcripts and themes derived from the data to ensure its accuracy as a second data source as well as confirm thematic analysis.

Data Analysis

According to Bradley, Curry, and Devers (2007), there is no singular way to conduct qualitative data analysis, although there is general agreement that the process is ongoing. An important first step is to immerse and comprehend the meaning (5). A modification of the van Kaam method of analysis for phenomenological data, which occurs through a multi-step process, was employed in the present study (24). This method identifies common themes and patterns used by participants in a qualitative research study.

The first step requires data to be organized, transcribed, and coded. Organization of data is critical in qualitative research because of the large amount of information gathered during the study (12). The data was organized by material type: all interviews, all observations, and all documents. Finally, data was coded.

The next step in the modified van Kaam data analysis method requires participants’ statements to be categorized, clustered, coded, and labeled into groups (24). The common themes constituting the core elements of the lived experiences of the participants were most important. Coding is a process of making sense of the data, dividing the data into text or image segments, labeling the segments with codes, examining codes for overlap and redundancy, and collapsing these codes into broad themes (12).

RESULTS

The premise of this study was to develop an understanding about the leadership skills of ADs with a particular focus on financial expertise. A semi-structured interview process was used to develop an overall analysis of expert thinking. The analysis revealed three emerging themes: (a) leadership, (b) roles and responsibilities, and (c) student-athletes. Each theme is explained and then supported by participant quotes.

Theme One: Leadership

With respect to leadership, leadership skills, types, and supervision were considered important. Participants mentioned the skills to self-evaluate and feedback and how important it was to reflect on their own performances. Self-evaluation is necessary in addition to soliciting feedback from others who might be able to provide insight. Participant 1 said,

I think through and self-evaluate, and each year I am evaluated by the Vice President and President of the college. The evaluation process also includes coaches, the trainer, and the secretary to find out what I need to improve on and set some goals.

Participant 12 stated, “Understanding my leadership skills involves listening to feedback and asking questions about how I am doing. A good leader must be open to constructive criticism and be a good listener and respect others’ opinions.”

The leadership of ADs may also influence the success of programs. According to Participant 6,

I am a leader by example as a positive person. I am reasonable and approachable, and [I] motivate with pride. I am a leader who likes to inspire others to be better. I am successful if our programs are. I want my coaches and student-athletes to be successful. I want to get the most out of people and care about what they are doing as followers.

Furthermore, Participant 3 said that

As a transformational leader, I look at the goals and vision of the athletic department and what needs to be done for the long term. Each athletic program has different needs and I look at the short and long term goals.

Theme Two: Roles and Responsibilities

A JC AD has multiple roles and responsibilities, but balancing budgets, securing funding, and distributing it appropriately was mentioned frequently. This is supported by Participant 6 who stated that, “Overseeing the budgets is a big part of my job. We have so much money for each program. Every program has a different number of student-athletes, coaches, etc. Each budget is different.”

Athletic directors must be able to budget well for each program they oversee. This is a challenge, as they must find ways to generate revenue to keep the programs active. For example, Participant 7 referred to fundraising.

Fundraising is the best way. I do not know of a community college that does not

fundraise. Most institutions cannot provide things such as backpacks or gear. There are strict rules about what can be purchased with state or district dollars. When there is a shortfall of funds, we have to fundraise to support the programs.

Participant 16 found that securing the necessary budget for JC athletics is frequently a challenge.

Money is very tight for athletic programs at community colleges. As a staff, we must fundraise to keep the programs going. The coaches fundraise for their sport. Some fundraising activities may be charity golf tournaments, barbeques, or bake sales.

Although finances are just one component of the responsibilities of an AD, it is apparent that they are a significant concern. For example, according to Participant 14, “The budget consumes 70% of my time to ensure the programs are run effectively.”

The decisions about athletic programs are a major responsibility for ADs. Participants reported that Title IX Gender Equity was a concern when adding, removing, or maintaining a program. “Title IX gender equity and compliance is a big issue, and we have to evaluate our athletic programs when considering adding or dropping a program”, said Participant 9. Participant 15, who stated that decisions about programs were made in consideration of Title IX and gender equity, supported this. Thus, it becomes a balancing act of meeting guidelines or policies while simultaneously ensuring that there is a sufficient budget.

I try to keep all my athletic programs. I try to make sure they are maintained with enough dollars coming in to keep them going. Terminating a program is the last thing I try to do. If nothing else, adding a program is a good thing but that takes money.

(Participant 16)

In JC athletics, things can change quickly, an AD must make decisions concerning their coaching staff who are responsible for the student-athlete. Thus, a change in a staff member may directly impact the athletic program and the student-athletes. According to Participant 4,

In athletics, change happens often. I deal with change by telling my coaches about changes and we work together on making changes when the time comes. Some people resist change, but change is a reality in athletics.

It is important, therefore, for the AD to be cognizant of upcoming change, and keep the staff apprised of changes that might impact them.

My coaches must deal with change the most because they spend the most time with the student-athletes. I teach them about change, when change is going to take place, how it affect their programs, and help them with change. Some adapt to change well, and others do not. I work with them all.

(Participant 8)

Theme Three: Student-Athletes

Some ADs reported the additional responsibility of having to coach. Although an AD wants to win both as a coach and director, there is recognition of balancing athletic success with academic success. In fact, the ADs placed academics above athletics. According to Participant 16, “The student-athlete should manage time by first looking at their academic responsibilities first then sports.” This is further supported by other examples.

The balance is placing academics ahead of athletics. The student-athlete must be organized and set up time schedules. A balanced student-athlete focuses toward academics and although athletics is important, earning good grades is equally important.

(Participant 14)

Athletic directors recognize that academic success is a reflection on the future prospects of the student-athlete, but also on the JC. Transferring to a larger institution is important for many students.

A student-athlete who cares about moving on beyond a two year college will do a good job with balancing academics and athletics. Although the student-athlete can do well in a sport, the student must have a good grade point average to transfer.

(Participant 8)

Motivation plays a big role in the student-athlete performance athletically and academically. The ADs are tasked with working with coaches to assist with motivating athletes. Just as a coach is a mentor to an athlete, the AD must serve as a mentor to the coach. According to Participant 13, “The athletic director sets the stage for the coaches to motivate the student-athletes.”

I try to promote morale and motivation with my coaches who are the leaders for the student-athlete. The coaches are mentors who motivate and inspire the student-athlete to good. As the athletic director I train the coaches to engage the student-athlete.

(Participant 2)

Some student-athletes are less self-motivated than others and require external motivation to perform better in a sport or academics. The ability to prioritize athletics and completing coursework with passing grades can be a challenge, yet “Increasing his or her self-motivation in the classroom can lead to a successful student-athlete” (Participant 11). Participant 6 noted that athletics has a tendency to be placed ahead of academics.

The challenged student-athlete lacks self-motivation, direction, and the ability to manage their time. This type of student-athlete lacks the passion for being engaged academically to learn in the classroom. They place athletics ahead of academics, which may be why they have difficulties earning good grades in the classroom.

DISCUSSION

The purpose of this qualitative, phenomenological study was to explore ADs lived experiences and perceptions of leadership in JC athletic programs particularly in reference to finances. Interview analysis revealed three main themes of leadership, roles and responsibilities, and the student-athlete. Each theme is discussed in light of current research.

Theme One: Leadership

Athletic directors recognized the importance of leadership in influencing the behavior and actions of others. According to Smith (1997), “As leaders face greater uncertainties and changes, and compounded complexities, they strive for greater flexibility and agility” (p. 277). In the present study, ADs saw their role as leaders encompassing a variety of roles and responsibilities as evidenced in the second theme. What is most important with these varying roles and responsibilities is the opportunity to receive feedback on their performance and make the appropriate adjustments based on the feedback received. “Effective leaders learn that comprehensive systematic reviews and evaluations should include every type of resource, every competency and capacity, and every person and position that affects performance” (33). Thus, some participants acquired evaluations from superiors, such as the college president or those working for the participant such as coaches, and applied this feedback to improve their leadership styles and effectiveness. Overall, the feedback an AD receives is a measuring tool for effectiveness in their role.

Theme Two: Roles and Responsibilities

Balancing budgets and securing funding was a clear concern for the participants. Many participants indicated that they were responsible for preparing the budget. A participative budget process involves lower-level administrators and coaches who better understand the individual line items who are responsible for the athletic department’s budget than senior administrators. A top down budgeting process offers short-term budgets imposed by senior administrators more likely to be consistent with the strategic long-term goals and objectives of the athletic department (20). Thus, those ADs expected to complete budgets without the use of participative budget methodology may experience higher levels of stress (32). Participative budgeting is supported by Wickstrom (2006), as an authoritative style of leadership is not conducive to the work force of the modern era, and that to be a successful leader an AD has to be willing to listen to those they lead.

The present study further found that gender equity and the budgetary requirements that stem from Title IX was considered both a financial and leadership challenge. This is not surprising, as gender equity at JCs has been clearly documented (8). A balance needs to exist between athletic sports programs relative to women’s sports and Title IX laws (19). Some ADs are faced with the decision to cut sports programs (Steinback, 2010) and must be cognizant of their current Title IX standing so that there does not become an imbalance of participation opportunities. Thus, there remains work to be done in achieving a standard of gender equity that not only meets the intent of Title IX but fully affords the respect of dignity for female student-athletes (19). As two-year athletic programs consider new directions, the achievement of gender equity within two year athletic programs still needs to be addressed (19), which is recognized by the participants of the present study.

Theme Three: Student-Athletes

The relationship that ADs had with student-athletes was an unexpected finding. This may be in part because some ADs reported the additional responsibility of serving as a coach. The extra coaching duties may cause additional stressors because it limits the time they have to devote to the financial responsibilities of the profession (21). Participants recognized that they were responsible with the coaches for improving both student athletic and academic performance. Participants stressed the importance of academics over athletics, but this may be due to efforts by the administration to increase retention and graduation rates (29). Not only did ADs report high levels of interaction with student-athletes, they generally viewed it as part of their responsibility to motivate the student to achieve both in athletics and in the classroom. That ADs viewed this as a component of their leadership was unexpected, as this task is frequently the responsibility of a coach or even assistant (15).

Limitations and Future Research

Although the present study provides some interesting findings, they should be evaluated with respect to its limitations. First, this study was limited to current full-time ADs at JCs in the state of California, which may not translate to the experiences of ADs in other locations or athletic conferences. Second, only four participants were female. This is not uncommon (1), and future research should consider whether opinions and perceptions differ between genders. For example, impressions of Title IX may differ by gender (1), and Title IX challenges may differ between JCs and traditional four-year institutions. Third, the specific financial expertise of each participant was not assessed. Therefore, future research should consider whether financial education and training improves AD financial expertise and progress toward short, intermediate, and long term strategic goals. The recommendation may benefit both low-level and senior level administrators at the JC. In addition, future researchers should consider conducting a broader survey of the general background and experiences of ADs in JCs.

CONCLUSIONS

The success of collegiate athletic programs can depend upon the skills of their ADs (31). Thus, they must possess leadership skills across multiple disciplines. Because financial and budgetary concerns were most prevalent among the participants of the present study, future research needs to investigate the training being provided for ADs. The financing and budget process is vital in ensuring that athletic programs are successful, and an action plan is needed for current and future ADs to use as a model to understand the entire financial and budget process of funding athletics programs.

APPLICATIONS IN SPORT

Empirical research has focused primarily on the Division I AD. However, these findings suggest that JC ADs encounter a variety of challenges which have not been investigated. JC administrators need to consider the budgetary and fundraising background and expertise of applicants, which is a paramount responsibility of ADs in JC.

ACKNOWLEDGMENTS

None

REFERENCES

1. Anderson, D. J., Cheslock, J. J., & Ehrenberg, R. G. (2006). Gender equity in intercollegiate athletics: Determinants of Title IX compliance Journal of Higher Education, 77, 225-250.

2. Barr, C. A., Hums, M. A., & Masteralexis, L. P. (2009). Principles and practice of sport management (3rd ed.). Sudbury, MA: Jones and Bartlett.

3. Berkowitz, S. (2011, June 28). Rutgers athletic department needs fees, funds to stay afloat. USA Today. Retrieved from http://usatoday30.usatoday.com/sports/college/2011-06-28-rutgers-athletic-department-subsidies_n.htm

4. Blanchard, K. (2010). Leading at a higher level: Blanchard on leadership and creating high performing organizations. Upper Saddle River, NJ: BMC, Blanchard Management Corporation.

5. Bradley, E. H., Curry, L. A., & Devers, K. J. (2007). Qualitative data analysis for health services research: Developing taxonomy, themes, and theory. Health Services Research, 42, 1758-1772.

6. Byrd, L. A., & Williams, M. R. (2007). Expansion of community college athletic programs. Community College Enterprise, 13, 39-49.

7. Caldwell, L., Creswell, J., & Iwamoto, D. K. (2007). Feeling the beat: The meaning of rap music for ethnically diverse Midwestern college students: A phenomenological study. Adolescence, 42, 337-351.

8. Castaneda, C., Hardy, D. E., & Kastinas, S. G. (2008). Meeting the challenge of gender equity in community college athletics. New Directions for Community Colleges, 142, 93-105.

9. Cohen, D., J., & Crabtree, B. F. (2008). Evaluation criteria for qualitative research in health care: Controversies and recommendations. Animals of Family Medicine, 6, 331-339.

10. Cooper, C., & Weight, E. (2011). Investigating NCAA administrator values in NCAA Division I athletic departments. Journal of Issues in Intercollegiate Athletics, 4, 74-89.

11. Creswell, J. W. (1994). Research design: Qualitative and quantitative approaches (1st ed.). Thousand Oaks, CA: Sage Publications, Inc.

12. Creswell, J. W. (2005). Educational research: Planning, conducting, and evaluating quantitative and qualitative research. (2nd ed.). Upper Saddle River, NJ: Pearson.

13. Davis, D. J. (2001). An analysis of the perceived leadership styles and levels of satisfaction of selected junior college athletic directors and head coaches. United States Sports Academy. Retrieved from Proquest, UMI Dissertations Publishing, 3026212.

14. Dunn, J. M. (2013). Should the playing field be leveled? Funding inequities among Division I athletic programs. Journal of Intercollegiate Sport, 6, 44-51.

15. Fitzgerald, M. P., Nelson, B., & Sagaria, M. D. (1994). Career patterns of athletic directors: Challenging the conventional wisdom. Journal of Sport Management, 8, 14-26.

16. Ferguson, L. (2004). External validity, generalizability, and knowledge utilization. Journal of Nursing Scholarship, 36, 16-22.

17. Giannotto, M. (2012, July 2). Maryland cuts seven sports on ‘sad day’ in College Park, Washington Post. Retrieved from http://articles.washingtonpost.com/2012-07-02/sports/35486395_1_athletic-programs-track-program-athletic-director-kevin-anderson

18. Golafshani, N. (2003). Understanding reliability and validity in qualitative research. Qualitative Report, 8, 597-607.

19. Hagedorn, L. S., & Horton D., Jr. (2009). Student athletes and athletics. New Directions for Community Colleges, 147, 1-91.

20. Hodge, F., & Tanlu, L. (2009). Finances and college athletics. New Directions for Institutional Research, 140, 7-18.

21. Judge, L. W., & Judge, I. L. (2009). Understanding the occupational stress of interscholastic athletic directors. ICHPER – SD Journal of Research in Health, Physical Education, Recreation, Sport & Dance, 4, 37-44.

22. Kirkpatrick, S. A., & Locke, E. A. (1991). Leadership: Do traits matter? Executive, 5, 48-60.

23. Lewis, B. A., & Quarterman, J. (2006). Why students return for a master’s degree in sport management. College Student Journal, 40, 717-728.

24. Moustakas, C. (1994). Phenomenological research methods. Thousand Oakes, CA: Sage Publications.

25. Mukamusoni, D. (2006). Distance learning program of teachers at Kigali institute of education: An expository study. International Review of Research in Open and Distance Learning, 3, 1-10.

26. Nahavandi, A. (2006). The art and science of leadership. Upper Saddle River, NJ: Pearson. Prentice Hall.

27. Nelson, B., & Rawlings, D. (2007). Its own reward: A phenomenological study of artistic creativity. Journal of Phenomenological Psychology, 38, 217-255.

28. Northouse, P. G. (2013). Leadership: Theory and practice. Thousand Oaks, CA: SAGE.

29. Ohlson, M., & Storch, J. (2009). Student services and student athletes in community colleges. New Directions for Community Colleges, 147, 75-84.

30. Robertson, J. E. (2008). Leadership, athletic directors and mental toughness. National Junior College Athletic Association Review, 60, 2-6.

31. Ruihley, B. J., & Fall, L. T. (2009). Assessment on and off the field: Examining athletic directors’ perceptions of public relations in college athletics. International Journal of Sport Communication, 2, 398-410.

32. Ryska, T. A. (2002). Leadership styles and occupational stress among college athletic directors: The moderating effect of program goals. Journal of Psychology, 136, 1-22.

33. Smith, A. W. (1997). Leadership is a living system: Learning leaders and organizations. Human Systems Management, 16, 277-284. Retrieved from ProQuest at http://search.proquest.ezproxy.apollolibrary.com/docview201129759?

34. Steinbach, P. (2010). Economic Storm. National Junior College Athletic Association Review, 62, 4-7.

35. Wickstrom, B. D. (2006). Message to ADs: Get to know donors. National Collegiate Athletic Association News, 43, 4-24.

36. Williams, M. R., Byrd, L., & Pennington, K. (2008). Intercollegiate athletics at the community college. Community College Journal of Research and Practice, 32, 453-461.

37. Zimbalist, A. (2013). Inequality in intercollegiate athletics: Origins, trends and policies. Journal of Intercollegiate Sport, 6, 5-24.

Submitted by C. Barry Pfitzner, Steven D. Lang and Tracy D. Rishel

ABSTRACT

In this paper we attempt to predict the total points scored in National Football League (NFL) games for the 2010-2011 season. Separate regression equations are identified for predicting points for the home and away teams in individual games based on information known prior to the games. The sum of the predictions for the home and away teams computed from the regression equations (updated weekly) are then compared to the over/under line on individual NFL games in a wagering experiment to determine if a successful betting strategy can be identified. All predictions in this paper are out-of-sample—meaning that all of the information necessary for the predictions was available before the games were played. Using this methodology, we find that several successful wagering strategies could have been applied to the 2010-2011 NFL season. We also estimate a single equation to predict the over/under line for individual games. That is, we test to see if the variables we have collected and formulated are important in predicting the betting line for NFL games. These results can be used by either bettors or bookmakers wanting to increase their odds of success in the gaming industry.

INTRODUCTION

Bookmakers set over/under lines for virtually all NFL games. Suppose the over/under line for total points in a particular game is 40. Suppose further that a gambler wagers with the bookmaker that the actual points scored in the game will exceed 40, that is, he bets the “over.” If the teams then score more than 40 points, the gambler wins the wager. If the teams score under 40 points, the gambler loses the bet. If the teams score exactly 40 points, the wager is tied and no money changes hands. The process works symmetrically for bets that the teams will score fewer than 40 points, or betting the “under.” The over/under line differs, of course, on individual games. Since losing bets pay a premium (often called the “vigorish,” “vig,” or “juice” and typically equal 10%), the bookmakers will profit as long the money bet on the “over” is approximately equal to the amount of money bet on the “under” (bookmakers also sometimes “take a position,” that is, they will welcome unbalanced bets from the public if the bookmaker has strong feelings regarding the outcome of the wager [see also the reference to Levitt’s work in the literature review]). It is widely known a gambler must win 52.4% of the wagers to be successful. That particular calculation can be established simply. Let Pw = the proportion of winning bets and (1 – Pw ) = the proportion of losing bets. The equation for breaking even on such bets where every winning wager nets $10 and each losing wager represents a loss of $11 is:

Pw ($10) = (1 – Pw ) ($11) , and solving for Pw

Pw = 11∕21 = .5238, or approximately 52.4%

This research attempts to identify methods of predicting the total points scored in a particular game based on information available prior to that game. The primary research question is whether or not these methods can then be utilized to formulate a successful gambling strategy for the over/under wager, with success requiring a winning percentage of at least 52.4%.

The remainder of this paper is organized as follows: in the next section we describe the efficient markets hypothesis as it applies to the NFL wagering market; we then offer a brief review of the literature; in the following section we describe the data and method; descriptive statistics and the main regression results are then presented; these are followed by the wagering simulations; we next discuss our investigation of the determinants of the over/under line; and finally offer our conclusions.

NFL Betting as a Test of the Efficient Markets Hypothesis

A number of important papers have treated wagering on NFL games as a test of the Efficient Market Hypothesis (EMH). This hypothesis has been widely studied in economics and finance, often with focus on either stock prices or foreign exchange markets. Because of the difficulties of capturing EMH conclusions given the complexities of those markets, some researchers have turned to the simpler betting markets, including sports (and the NFL), as a vehicle for such tests.

If the EMH holds, asset prices are formed on the basis of all information. If true, then the historical time series of such asset prices would not provide information that would allow investors to outperform the naïve strategy of buy-and-hold (see, for example, Vergin 2001). As applied to NFL betting, if the use of past performance information on NFL teams cannot generate a betting strategy that would exceed the 52.4% win criterion, the EMH hypothesis holds for this market. Thus, the thrust of much of the research on the NFL has taken the form of attempts to find winning betting strategies, that is, strategies that violate the weak form of the EMH.

A Brief Review of the Recent Literature

Nearly all of the extant literature on NFL betting uses the point “spread” as the wager of interest. The spread is the number of points by which one team (the favorite) is favored over the opponent (the underdog). Suppose team A is favored over team B by 7 points. A wager on team A is successful only if team A wins by more than 7 points (also known as “covering” the spread). Symmetrically, a wager on team B is successful only if team B loses by fewer than 7 points or, of course, team B wins or ties the game—in any of these cases, team B “covers.” Vergin (2001) and Gray and Gray (1997) are examples of research that focus on the spread.

Based on NFL games from 1976 to 1994, Gray and Gray (1997) find some evidence that the betting spread is not an unbiased predictor of the actual point spread on NFL games. They argue that the spread underestimates home team advantage, and overstates the favorite’s advantage. They further find that teams who have performed well against the spread in recent games are less likely to cover in the current game, and those teams that have performed poorly in recent games against the spread are more likely to cover in the current game. Further Gray and Gray find that teams with better season-long win percentages versus the spread (at a given point in the season) are more likely to beat the spread in the current game. In general, they conclude that bettors value current information too highly, and conversely place too little value on longer term performance. That conclusion is congruent with some stock market momentum/contrarian views on stock performance. Gray and Gray then use the information to generate probit regression models to predict the probability that a team will cover the spread. Gray and Gray find several strategies that would beat the 52.4% win percentage in out-of-sample experiments (along with some inconsistencies). They also point out that some of the advantages in wagering strategies tend to dissipate over time.

Vergin (2001), using data from the 1981-1995 seasons, considers 11 different betting strategies based on presumed bettor overreaction to the most recent performance and outstanding positive performance. He finds that bettors do indeed overreact to outstanding positive performance and recent information, but that bettors do not overreact to outstanding negative performance. Vergin suggests that bettors can use such information to their advantage in making wagers, but warns that the market and therefore this pattern may not hold for the future.

A paper by Paul and Weinbach (2002) is a departure from the analysis of the spread in NFL games. They (as do we in this paper) target the over/under wager, constructing simple betting rules in a search for profitable methods. These authors posit that rooting for high scores is more attractive than rooting for low scores. Ceteris paribus, then, bettors would be more likely to choose “over” bets. Paul and Weinbach show that from 1979-2000, the under bet won 51% of all games. When the over/under line was high (exceeded the mean), the under bet won with increasing frequency. For example, when the line exceeded 47.5 points, the under bet was successful in 58.7% of the games. This result can be interpreted as a violation of the EMH at least with respect to the over/under line.

Levitt (of Freakonomics fame) approaches the efficiency question from a different perspective. It is clear that if NFL bets are balanced, the bookmaker will profit by collecting $11 for each $10 paid out. As we suggested earlier, bookmakers at times take a “position” on unbalanced bets, on the assumption that the bookmaker knows more about a particular wager than the bettors. Levitt presents evidence that the spread on games is not set according to market efficiency. For example, using data from the 2001-2002 seasons, he shows that home underdogs beat the spread in 58% of the games, and twice as much was bet on the visiting favorites. Bookmakers did not “move the line” to balance these bets, thus increasing their profits as the visiting favorite failed to cover in 58% of the cases.

Dare and Holland (2004) re-specify work by Dare and MacDonald (1996) and Gray and Gray (1997) and find no evidence of the momentum effect suggested by Gray and Gray, and some, but less, evidence of the home underdog bias that has been consistently pointed out as a violation of the EMH. Dare and Holland ultimately conclude that the bias they find is too small to reject a null hypothesis of efficient markets, and also that the bias may be too small to exploit in a gambling framework.

Still more recently, Borghesi (2007) analyzes NFL spreads in terms of game day weather conditions. He finds that game day temperatures affect performance, especially for home teams playing in the coldest temperatures. These teams outperform expectations in part because the opponents were adversely acclimatized (for example, a warm weather team visiting a cold weather team). Borghesi shows this bias persists even after controlling for the home underdog advantage.

METHODS

We focus on the total points scored in NFL games and the corresponding over/under line for that game. With the objective of estimating regression equations for home and away team scoring, data were gathered for the 2010-11 season for the analysis. The variables include:

TP = total points scored for the home and visiting teams for each game played

PO = passing offense in yards per game

RO = rushing offense in yards per game

PD = passing defense in yards per game

RD = rushing defense in yards per game

GA = “give aways,” offensive turnovers per game

TA = “take aways,” defensive turnovers per game

D = a dummy variable equal to 1 if the game is played in a closed dome, 0 otherwise

PP = points scored by a given team in their prior game

L = the over/under betting line on the game

Match-ups Matter (we think)

The general regression format is based on the assumption that “match ups” are important in determining points scored in individual games. For example, if team “A” with the best passing offense is playing team “B” with the worst passing defense, ceteris paribus, team “A” would be expected to score many points. Similarly, a team with a very good rushing defense would be expected to allow relatively few points to a team with a poor rushing offense. In accord with this rationale, we formed the following variables:

PY = PO + PD = passing yards

RY = RO + RD = rushing yards

For example, suppose team “A” is averaging 325 yards (that’s high) per game in passing offense and is playing team “B” which is giving up 330 yards (also, of course, high) per game in passing defense. The total of 655 would predict many passing yards will be gained by team “A,” and likely many points will be scored by team “A.”

Similarly, we theorize that if a team’s offense that commits many turnovers plays a team whose defense causes many turnovers, points scored for the offensive team may be lower (and perhaps more points will be scored by the defensive team). For turnovers, we created variables similar to the passing and rushing yards in the previous paragraph:

TO = GA + TA, that is, turnovers = “give aways” for a given team plus “take aways” for the opposition team.

The dome variable will be a check to see if teams score more (or fewer) points if the game is played indoors.

The variable for points scored in the prior game (PP) is intended to check for streakiness in scoring. That is, if a team scores many (or few) points in a given game, are they likely to have a similar performance in the ensuing game?

We also test to ascertain whether or not scoring is contagious. That is, if a given team scores many (or few) points, is the other team likely to score many (or few) points as well? We test for this by two-stage least squares regressions in which the predicted points scored by each team serve as explanatory variables in the companion equation.

General Regression Equations

The general sets of regressions attempted are of the form: where the subscripts h and v refer to the home and visiting teams respectively, and the i subscript indicates a particular game.

Equations such as 1 and 2 are estimated using data for weeks 5 through 17 of the 2010-11 season. We chose to wait until week five to begin the estimations so that statistics on offense, defense, turnovers, etc., are more reliable than would be the case for earlier weeks.

RESULTS AND DISCUSSION

Descriptive Statistics

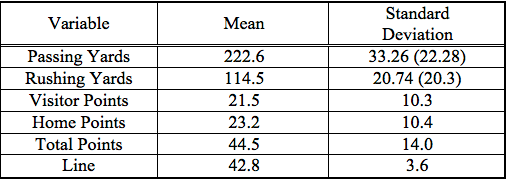

Table I contains some summary statistics for the data set. Teams averaged approximately 223 yards passing per game (offense or defense, of course) for the season, and they averaged approximately 115 yards rushing. The statistics reported on the rushing and passing standard deviations without parentheses are for the offenses and the defensive standard deviations are (as you might guess) in parentheses. Interestingly, passing defense is less variable across teams than is passing offense (we hypothesize that teams must be more balanced on defense to keep other teams from exploiting an obvious defensive weakness, but teams may be relatively unbalanced offensively and still be successful [see the 2011 Packers, for example, who ranked near the top in passing offense and near the bottom in rushing defense]). Home teams scored approximately 23.2 points on average for the season and outscored the visitors by 1.7 points. Total points averaged 44.5 in 2010-2011 and the over/under line averaged 42.8 (the difference between these means is statistically significant at α < .10; the calculated value for the t-test of paired samples is approximately 1.92). Not surprisingly, the standard deviation was much smaller for the line than for total points.

Table I: Summary Statistics

Regression Results

Though equations 1 and 2 from above represent our theoretical foundation, we did not find empirical support for the dome effect, points scored in the prior game, or for turnovers in predicting points for either the home or away teams. Thus we do not report regressions with those variables included (such estimations are available from the authors upon request). Since our objective is to produce predictions based on variables (and their effects) that are known prior to the games, we updated the equations weekly and checked for effects for those excluded variables. We did not find convincing evidence that any of the excluded variables should be included in the predictive equations.

The dome effect in a previous paper (see Pfitzner, Lang, & Rishel, 2009) found that teams scored approximately 5.4 more points when the game was played in a closed dome stadium for the 2005-2006 season. However, for the 2010-2011 season, games played in domes averaged 45.4 points and games played outdoors averaged 44.3. That difference is not statistically significant; the t-test for independent samples yields a calculated value of 0.54. The dome effect may be idiosyncratic in that, in some seasons, the high scoring teams may happen to be those who play home games in domed stadiums.

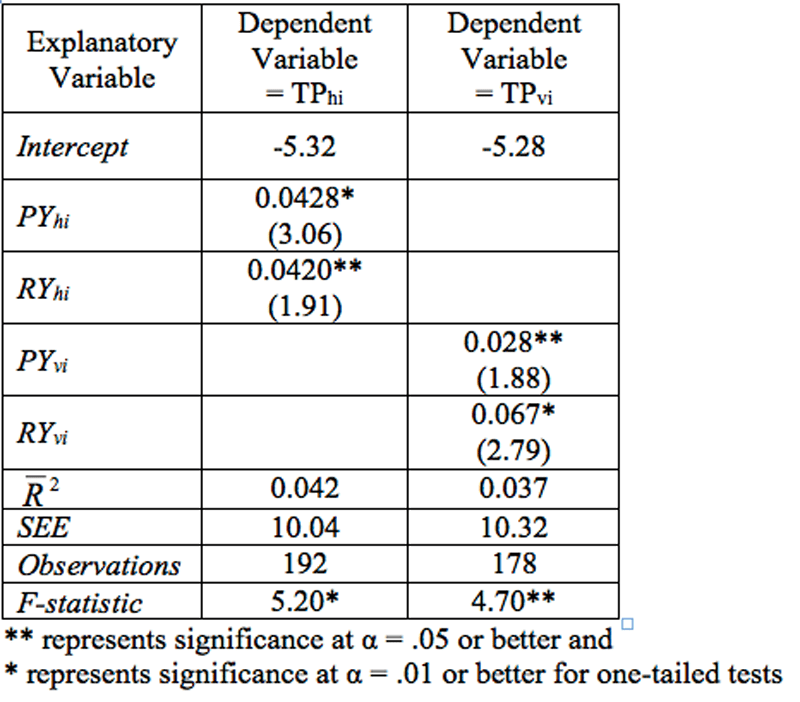

The representative estimated equations (at the end of the 16th week) are given in Table II. For the home points equation, the passing yardage and the rushing yardage are significant at α < .01, and α < .05 levels, respectively. The equation explains a modest 4.2% ( ) of the variance in home points scored. On the other hand, the F-statistic indicates that the overall equation meets the test of significance at α < .01. The estimated coefficients for the variables have the anticipated signs. To interpret those coefficients, an additional 100 yards passing (recall that this is the sum of the home team’s passing offense and the visitor’s passing defense) implies approximately 4.3 additional points for the home team, whereas an additional 100 yards rushing implies approximately 4.2 additional points.

Table II: Regression Results for Total Points Scored

The visiting team estimation yields a similar equation in terms of the overall fit. The explanatory variables are statistically significant—the passing yardage variable at α < .05, and the rushing yardage variable is significant at α < .01. The equation explains only 3.7% ( ) of the variance in visiting team points, and the F-statistic implies overall significance at α < .05. The coefficients perhaps suggest a more important role for rushing than for passing in scoring for the visiting team. If the coefficients are to be believed, an additional 100 yards passing yields approximately 2.8 points for the visiting team, and an additional 100 yards rushing is worth 6.7 points.

The reader may find such low values to be of concern, but recognize that the variables for which we are attempting estimates are very difficult to predict and are subject to wide variation. As we show in a later section, the lines on the games are much easier to predict. The model is best judged by its prediction qualities—here based on wagering success.

Other Hypotheses

Another hypothesis we wished to entertain is whether or not scoring is contagious. A priori, we surmised that points scored in given games for visiting and home teams would be positively related. In keeping with our earlier work, there is no evidence that such is the case. The estimated simple correlation coefficient between home team and visiting team points is -0.106, which is not statistically different from zero and “wrong” signed according to our intuition. Our initial thinking was that if team “A” scores and perhaps takes a lead, team “B” has greater incentive to score. An obvious complicating factor is that a given team may dominate time of possession, thus preventing the opposing team opportunities to score. We also experimented with two-stage least squares to test the hypotheses that scoring was contagious. In that formulation we developed a “predicted points” variable for the home team, entered that variable as an independent variable in the visiting team equation, and reversed the procedure for the home team equation. Neither of the predicted points variables were statistically significant. The variable was positively signed for the home team equation, and negatively signed for the away team equation.

As indicated above, we also find no evidence that teams are “streaky” with respect to points scored. In short, we find that points scored in the immediately prior week do not contribute to the explanation of points scored in the current week. That conclusion holds up for the regressions in section VI as well.

Finally, though turnovers clearly matter in who wins or loses, there is no evidence from our work that measuring teams’ turnovers per game prior to the current game aids in predicting points scored by the individual teams.

Wagering on the Over/Under Line

In this simulated wagering project we use the estimated equations to predict scores of the home and away teams for all of the games played over weeks 8 through week 17 (end of the regular season). The points predicted in this manner are then compared to the over/under line for each game. We then simulate betting strategies on those games.

Out-of-Sample Method

Since it is widely known that betting strategies that yield profitable results “in sample,” are often failures in “out-of-sample” simulations, we use a sequentially updating regression technique for each week of games. Suppose, for example, we are predicting points for week 8. We then estimate equations TPhi and TPvi with the data from weeks 5, 6, and 7, then “feed” those equations with the known data for each game through the end of week 7, generating predicted points for the visiting and home team for all individual games in week 8. The predicted points are then totaled and compared to the over/under line for each game. Next we add the data from week 8, re-estimate equations TPhi and TPvi, and make predictions for week 9. The same updating procedure is then used to generate predictions for weeks 10 through 17. This method ensures that our results are not tainted with in-sample bias.

Betting Strategies

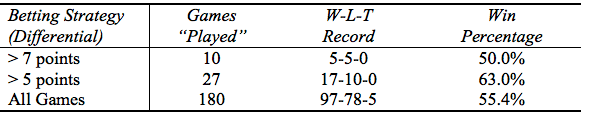

We entertain three betting strategies for the predicted points versus the over/under line on the games. These strategies are:

1. Bet only games for which our predicted total points differ from the line by more than 7 points.

2. Bet only games for which our predicted total points differ from the line by more than 5 points.

3. Bet all games for which our predicted total points differ from the line by any amount—in our case, all games.

As stated previously, a betting strategy on such games must predict correctly at least 52.4% of the time to be successful. If a given method cannot beat this 52.4% criterion, as a betting strategy it is deemed to be a failure.

Table III contains a summary of the results for the three betting strategies. The first betting strategy yields only ten “plays” over weeks 6 to 17. That betting strategy would have produced five wins, and five losses. For this (very) small sample, this strategy is, of course, not profitable, with only a 50% winning percentage. The second strategy (a differential greater than 5 points) yields 39 plays and a record of 17-10-0—a winning percentage of 63%. Finally for every game played, the method produces a still profitable record of 97-78-5, with the winning percentage at 55.4%.

Table III: Results of Different Betting Strategies

There is some consistency between these results and those we found for the 2005-2006 season. In that work we found that the “> 5 points” strategy produced a winning percentage of 60.5% based on 39 plays. Betting all games produced a winning percentage of 54%. Interestingly, the earlier research produced nine games with a greater than 10 point difference between the line and the predicted points whereas this work on 2010-2011 season produced only one play (which would have been a winning bet).

It is important to note that we make no adjustment for injuries, weather, and the like that would be considered by those who make other than simulated wagers. We offer these methods only as a guide, not as a final strategy.

Another Method of Predicting the Line and Total Points

Since we have collected and created variables that may be relevant to determining the betting line (and total points), in this section we investigate the relevancy of our variables in that context. For purposes of comparison, we estimate an equation for the over/under line and, separately, for the actual points scored. Further, we compare the results for the 2010-11 season with our results from prior research. These equations may be useful in confirming (or contradicting) the results of the previous sections, and may provide useful information applicable to wagering strategies.

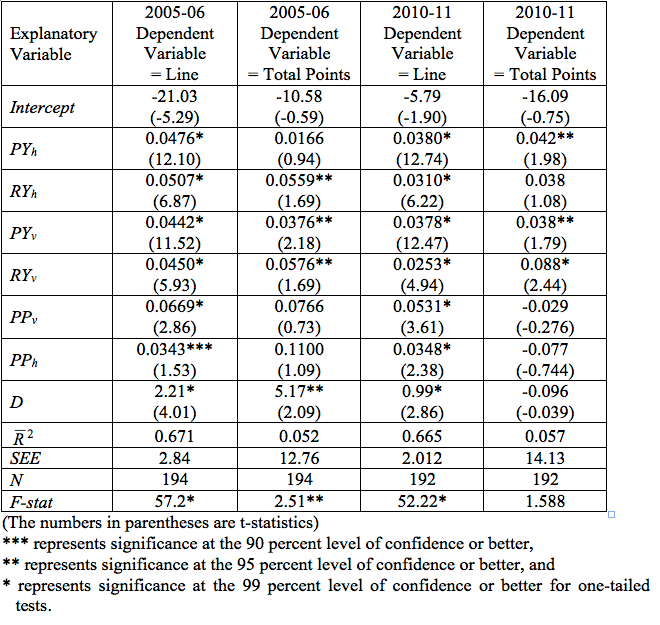

The results of those regressions are contained in Table IV. We estimated regression equations for two seasons with the line as the dependent variable and all of the right-hand side variables (with the exception of turnovers) specified in equations 1 and 2. The estimations for the line are contained in the second column (2005-2006 season) and the fourth column (2010-2011 season). The estimations are remarkably similar. For the line for both seasons, every coefficient estimate is correctly signed and statistically significant at traditional levels of alpha, and for both equations. The line seems to be set on the assumption that teams are streaky (we conclude they are not), and the dome effect on the betting line seems to be a bit smaller in the most recent season.

Table IV: Regression Results for the Line and Total Points, 2005 and 2010 Seasons

As a comparison, we also estimated (far less successfully) an equation for total points with the same set of explanatory variables with those results reported in columns three and five of Table IV. Perhaps the most striking result of these regressions is that the regressions for the line explain fully two-thirds of the variance in that dependent variable and the equations for the actual points explains less than 6% of the variance in total points for either season, with only four of the seven explanatory variables meeting the test for statistical significance at traditional levels for 2005-2006 and only three for 2010-2011. Interestingly, the dome effect for total points for the earlier season estimated 5 additional points scored in dome games, and the corresponding estimate for the 2010-11 season was zero, when controlling for other effects. Recall that for the 2005-2006 season, 5.4 points more were scored in games played in domes, and the corresponding difference was only one point for the 2010-2011 season.

In short, and to be expected, the line is much easier to predict than is actual points scored. That is, the outcome of the games and points scored therein are not easily predicted. It is tempting to say, “That’s why they play the games.” At least two further observations are in order. First, consider the coefficients for points scored in the previous game. Those variables matter as would be anticipated on an a priori basis in determining the line for the game. However, they seem to play an insignificant (statistical or practical) role determining the actual points scored. This particular result may be interpreted as bettors placing too much emphasis on recent information, as other authors have suggested.

Finally, it also seems clear that the effect of playing indoors has dissipated between the two seasons for which we report results in Table IV. As we have emphasized, this may be simply the effect of teams who play many games indoors having poorer scoring teams for any particular year.

CONCLUSIONS

The regression results in this paper identify promising estimating equations for points scored by the home and away teams in individual games based on information known prior to the games. In a regression framework, we apply the model to three simulated betting procedures for NFL games during weeks 6 through 17 of the 2010-2011 season. Betting strategies based on the differences between our predictions and the over/under line produced profitable results for either all games at any differential or those for which our predictions differed from the betting line by 5 or more points.

Based on our earlier results finding profitable wagering strategies for the 2005-2006 season, we (and others) questioned whether these results will hold up in other seasons. Based on the results presented here—so far, so good.

APPLICATIONS IN SPORT

Betting on sports, the NFL in particular, is a very popular pastime among sports (or gambling) enthusiasts and a very lucrative business for bookmakers in Las Vegas and elsewhere. This research was conducted to determine whether successful wagering strategies could be developed based on regression equations used to predict points for the home and away teams in individual games. The sum of the predictions for the home and away teams, updated weekly, were then compared to the over/under line on individual NFL games. Certain betting strategies were identified as successful, and could therefore be used by those wanting to improve their odds while enjoying and increasing their interest in America’s favorite sport.

ACKNOWLEDGMENTS

None

REFERENCES

1. Badarinathi, R., & Kochman, L. (2001). Football betting and the efficient market hypothesis. The American Economist, 40(2), 52-55.

2. Borghesi, R. (2007). The home team weather advantage and biases in the NFL betting market. Journal of Economics and Business, 59, 340-354.

3. Boulier, B. L., Steckler, H. O., & Amundson, S. (2006). Testing the efficiency of the National Football League betting market. Applied Economics, 38, 279-284.

4. Dare, W. H., & Holland, A. S. (2004). Efficiency in the NFL betting market: modifying and consolidating research methods. Applied Economics, 36, 9-15.

5. Dare, W. H., & MacDonald, S. S. (1996). A generalized model for testing home and favourite team advantage in point spread markets. Journal of Financial Economics, 40, 295-318.

6. Gray, P. K., & Gray, S. F. (1997). Testing market efficiency: Evidence from the NFL sports betting market. The Journal of Finance, LII(4), 1725-1737.

7. Levitt, S. D. (2002). How do markets function? An empirical analysis of gambling on the National Football League. National Bureau of Economic Research (Working Paper No. 9422).

8. Paul, R. J., & Weinbach, A. P. (2002). Market efficiency and a profitable betting rule: Evidence from totals on professional football. Journal of Sports Economics, 3, 256-263.

9. Pfitzner, C. B., Lang, S. D., & Rishel, T. D. (2009). The determinants of scoring in NFL games and beating the over/under ;ine. New York Economic Review, 40, 28-39.

10. Pfitzner, C. B., Lang, S. D., & Rishel, T. D. (2006). Can regression help to predict total points scored in NFL games? In A. Avery (Ed.), The 2006 Southeastern INFORMS Conference Proceedings (pp. 312-317). Myrtle Beach, SC: Southeastern INFORMS.

11. Vergin, R. C. (2001). Overreaction in the NFL point spread market. Applied Financial Economics, 11, 497-509.

Submitted by Martin J. Greenberg and Thom Park, Ph.D.

INTRODUCTION

A “coach” is dictionary defined as one who trains intensively by instruction, demonstration, and practice. That dictionary definition may have defined the coach of old, but does not recognize the current job environment and employment conditions of the modern-day college coach. The college coach of today is required not only to be an instructor, but also act as a fund raiser, recruiter, academic adviser, public figure, budget director, television, radio and internet personality, alumni glad-handler, and any other role that the university’s athletic director or president may direct him to do. Sports sociologists would opine that college coaches suffer from a condition known in the social science discipline as ‘role strain;’ that is, they have far too many roles to fill at very high levels of performance.

Coaching is a high-profile and high-risk position where every move and moment is surrounded by stress, and every decision, whether on or off the field, is subject to second-guessing and scrutiny and may often be the subject of a vicious public debate. Job security is as fleeting as the last seconds of a basketball victory in an environment where employment contracts are broken as easily as made.

Twenty-five years ago the average tenure of a Division 1A Head Football Coach was about 2.8 years. Nothing has changed. The first day on the job must often be spent planning for the last day, as the back end of the contract, i.e. termination provisions, may be more important than the compensation package. Job continuance is often conditioned on winning because wins are the equivalent of the bottom line — putting fans in the stands, selling enhanced seating, bolstering alumni contributions, generating lucrative TV and cable contracts, qualifying for Bowl competition, and persuading recruits to accept scholarships.

It is no wonder why big time college coaches are compensated the way they are — the job environment dictates the high compensation level.

CEOs IN HEADPHONES

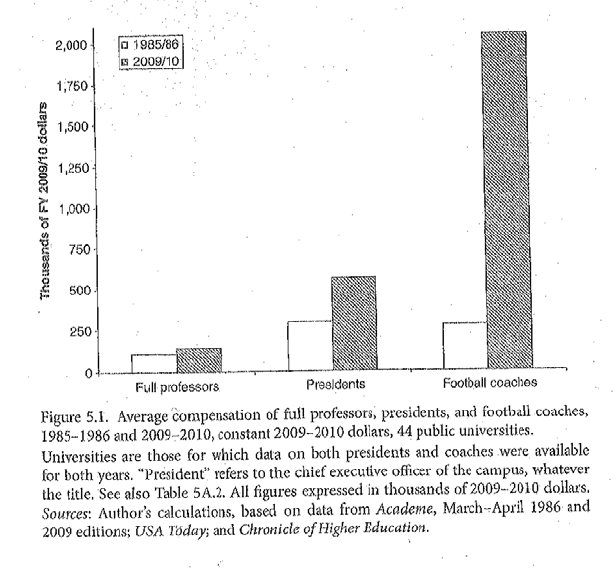

Today’s major college coaches are CEOs in Headphones. Components of their compensation in some ways equate to the CEOs of private or publicly held companies. Compensation packages can include a signing bonus, base pay and supplemental payments, loans, supplemental insurance, deferred compensation, annuities, memberships, company car, tuition, and golden parachute provisions, to name a few. It has been reported that during the period 2007 through 2011, CEO pay rose 23%, while in the same period college coaches’ pay increased 44%.

Coaches’ salary inflation is part of the athletics arms race and has run rampant. In a recent study, college coaching salaries rose more than 750% during the 24-year period between 1985 and 2010, while during the same period, pay for full professors increased 32%, and the pay for college presidents increased 90%.

In a survey conducted by the Knight Commission in 2009, 85% of university presidents believed that college football coaches’ compensation is excessive and identified escalating coaching salaries as the single largest contributing factor to the unsustainable growth of athletic spending.

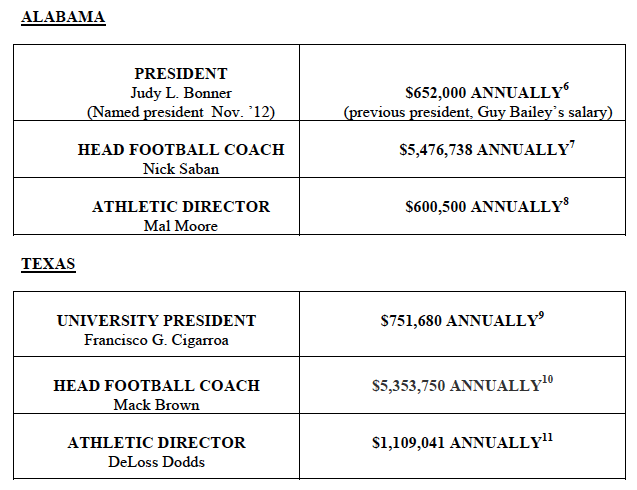

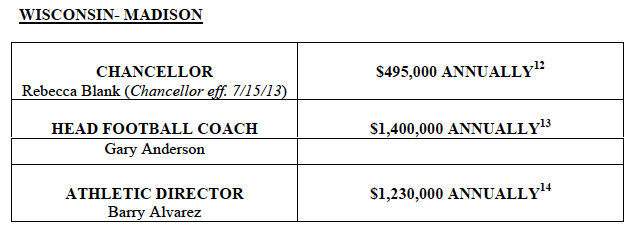

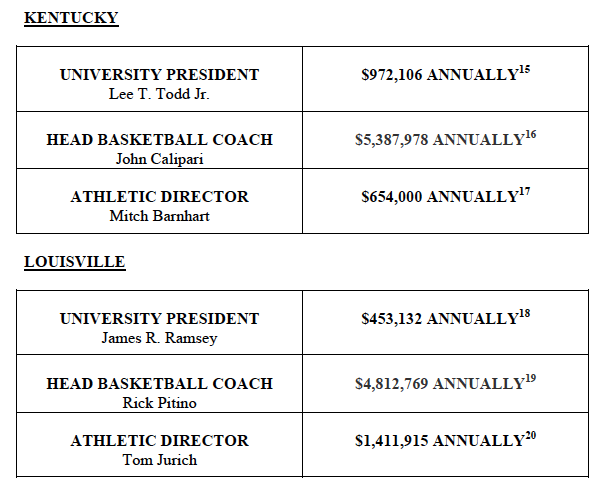

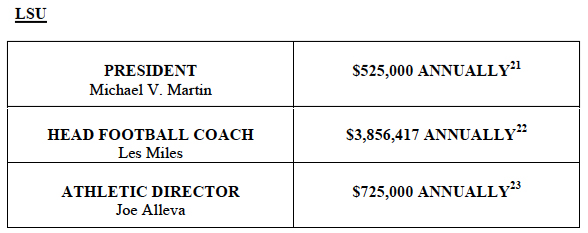

In most instances the college coach is the highest paid state employee of a public institution, and the compensation package can be five to ten times the amount paid university presidents and athletic directors. What follows is a comparison of reported, but unverified, compensation packages of presidents, head football coaches, and athletic directors at several major state schools:

COACH’S COMPENSATION

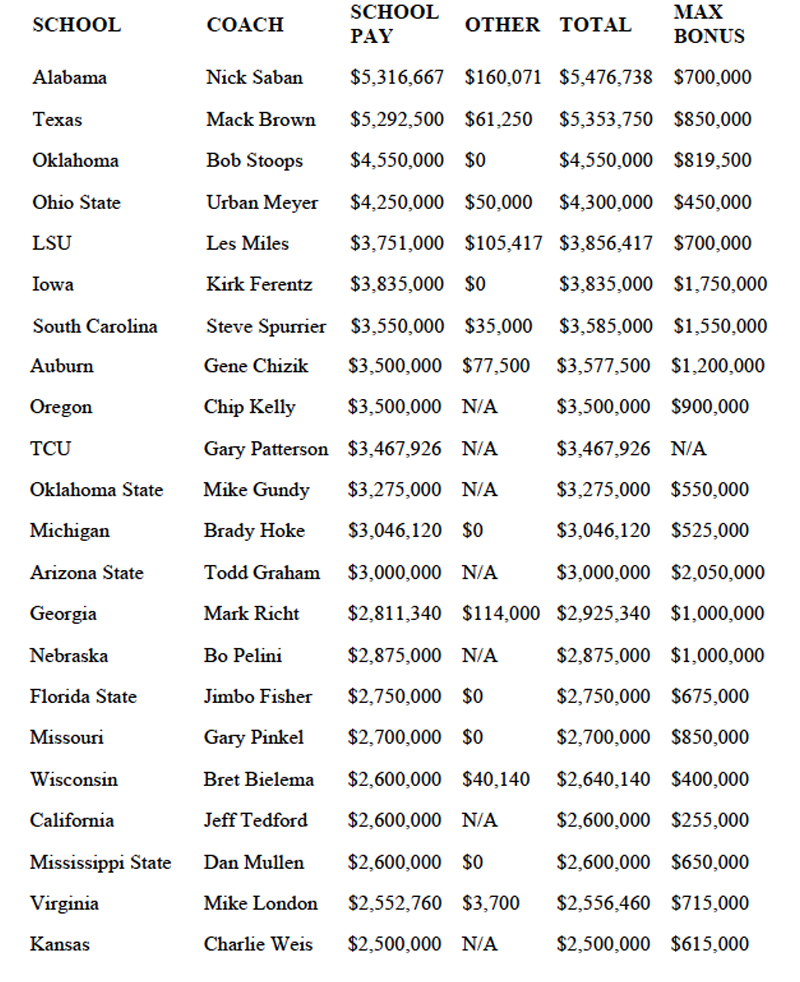

It was reported by USA Today that the average 2012 annual compensation for major college football head coaches is $1.64 million, up nearly 12% over the 2011 season, and more than 70% since 2006. Alabama’s Nick Saban and Texas’ Mack Brown are the highest paid football coaches.

The conference with the highest average compensation for its head football coaches is the Big 12, whose ten coaches are earning slightly less than $3 million a year. What follows, according to USA Today, are football coaches who earned at least $2.5 million for the 2012 football season:

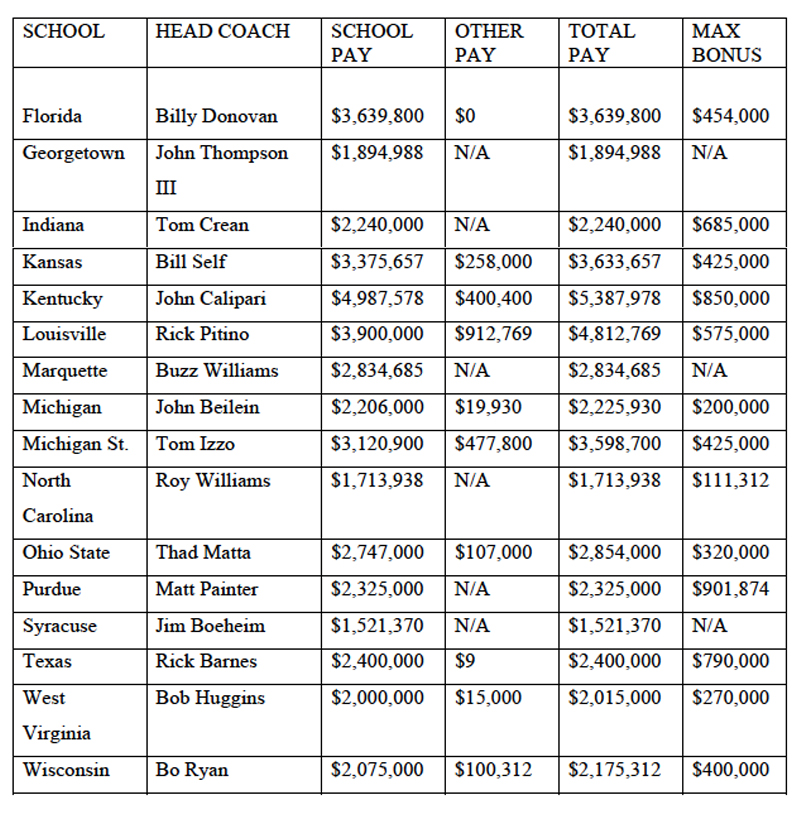

Similarly, the reported compensation packages, according to USA Today, of coaches for

major basketball programs are also healthy:

NCAA College Basketball Coaches’ Salary Database

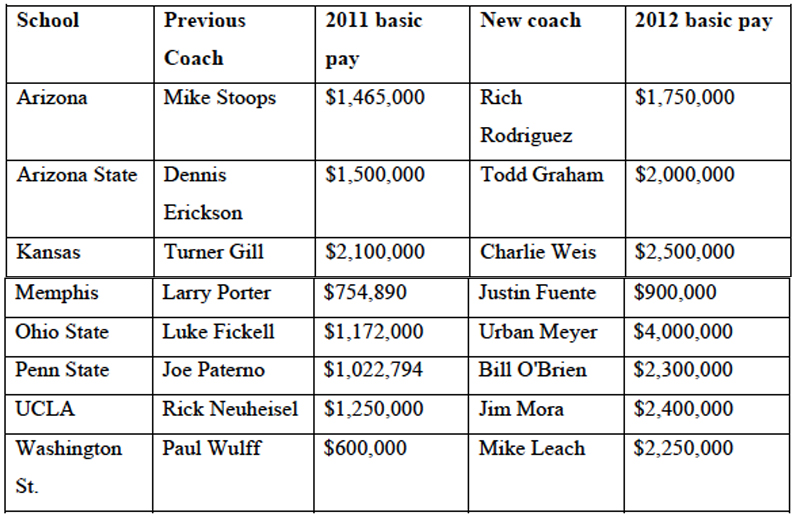

Among the 120 Bowl Division schools, 25 had made coaching changes for the 2012 season. Many of those universities who have made changes have had to dramatically increase their compensation packages in order to obtain their newly appointed coach.

OVERCOMPENSATED

So is a major college football coach overcompensated? There is no business like show business except $portsBiz. One in a million deserves more than a million. Compensation packages are market driven, and today the market is overly aggressive. The coaches’ market may not even be based on Moneyball Metrics, i.e. wins, tournament appearances and wins, revenue, attendance, rankings, or donations. A successful collegiate football program has many economic as well as non-economic benefits to the University, including driving alumni contributions and student enrollment, creating revenue streams that support non-revenue sports, and the psychic income of being “Big Time.” In many instances these escalating compensation packages are paid for through multi-million dollar paydays from conference broadcast and multi-media contracts, rabid fans willing to pay the price for enhanced seating, marketing deals with companies willing to sponsor the athletic initiative, apparel companies desirous of having their logo on athletes’ uniforms, and semi-autonomous booster clubs.

No comparative faculty member vs. athletic coach compensation analysis has ever taken into consideration the many other variables in the job life of the coach versus the job life of a faculty member. Some of these considerations and mitigating factors are job tenures, hours worked, stress endured, measured job pressure, frequency of termination versus tenured jobs, fractured unvested pension plans, lateral moves to advance, and the list goes on. By any measure, such compensation analyses versus the public perception of the coaches’ compensation are gravely misunderstood. College coaches earn absolutely every penny they make.

Universities are tasked with education, academic research, and public service to their communities. Coaches’ compensation packages that so dramatically dwarf the compensation packages of administrators and our best professors seems out of proportion. Even presidents and trustees of major universities can fall prey to the glamour of a winning season or a BCS bowl bid. In the context of amateurism, college athletes are not paid and big money can be targeted for a big name coach. The compensation packages of today’s college coaches are indicative of the high premium American society puts on the athletic enterprise. A successful college coach is a limited commodity, and the compensation packages are simply a function of supply and demand.

PACKAGE

For years we have negotiated the components of coaches’ compensation in reference to “The Package.” The Package included: I. Institutional Pay + Fringe Benefits

1. Salary

2. Life and health insurance

3. Vacation with pay

4. TIAA I CREF

6. Tuition waivers

6. Complimentary tickets

7. Annuity — longevity bonus

8. Contractual Bonuses

II. Outside income

1. Shoe, apparel, and equipment endorsements

2. Television, radio, and Internet shows

3. Speaking engagements

4. Personal or public appearances

5. Summer camps

III. Perquisites

1. Housing allowances

2. Membership in clubs

3. Business opportunities

4. Automobile usage

5. Dependent travel

6. Moving allowances

7. Additional insurance

8. Interest-free loans

The coach in most instances was permitted to separately contract for outside income sources. Today this is mostly university controlled and the coach receives institutional pay, plus fringe benefits, plus a talent fee or personal service fee that encompasses what previously was outside income but now is under institutional control, plus the perquisites as part of a total compensation package.

FINANCIAL ENGINEERING

The modern day coach financial structuring looks more like a CEO of a publicly traded or private company, with many new financial instruments and packages coming to the negotiation table including:

1. Signing bonuses

2. Retention, continuation, longevity bonuses

3. Up step life insurance provisions

4. Deferred compensation

5. Buyout of previous employer

6. Post-coaching employment

7. Interest free or forgivable loans

8. Retirement plans

9. Annuity

10. Expense account

11. Relocation payment

12. Disability payment

13. Entrepreneurial sharing

1. SIGNING BONUSES

BROWN – University of Texas-Austin: Special One Time Payment. Within 30 days of his execution of this agreement, Brown will receive a Special One Time Payment of $100,000.

JOHNSON – Georgia Tech: Signing Bonus. The Association agrees to pay Coach a onetime bonus of Two Hundred Thousand dollars ($200,000.00) within thirty (30) days of the signing of this employment contract.

MILLER – University of Arizona: Signing payment. As a consideration for the execution of this Contract, University will pay Coach one Million and 00/100 Dollars ($1,000,000) upon execution hereof.

MUSCHAMP – University of Florida: Signing Incentive. The Association shall pay to the Coach a Seven Hundred Fifty Thousand dollars ($750,000.00) signing incentive to be paid, subject to applicable taxes and withholding, upon execution and delivery of this Agreement by both parties.

O’LEARY – University of Central Florida: The coach shall be entitled to a signing bonus of $150,000 effective July 1, 2006, payable on next regularly scheduled Association pay period.

DYKES – University of California-Berkeley: Coach shall receive a one-time signing bonus of $594,000 on or before February 15, 2013.

2. RETENTION, CONTINUATION, LONGEVITY BONUSES

BARNES – University of Texas/Austin: If Barnes is head coach on March 31, 2010, a special payment of $1,000,000 will be made to Barnes. If Barnes is head coach on March 31, 2013, a second special payment of $1,000,000 will be made to Barnes.

CALIPARI – University of Kentucky: Retention Incentive. In addition to the above stated competitive and academic-based incentives, a retention incentive to encourage Coach to remain with the University shall be provided. University agrees to pay Coach a retention incentive if Coach remains in the employment of the University on each of the following dates:

March 31, 2014 (Bonus = $750,000), March 31, 2015 (Bonus = $1,000,000) and March 31, 2016 (Bonus + $1,250,000). Said bonuses to be paid within ten (10) days of the achievement of the applicable bonus.

DANTONIO – Michigan State University: 3.10. Contingent Annual Bonus. The University shall pay to Coach an annual bonus of Two Hundred Thousand Dollars ($200,000), provided that the Coach has served continuously as the Program Head Coach for the twelve consecutive months immediately preceding July 1st of the year in which the bonus will be paid. Such bonus will vest on the first business day following the conclusion of the twelve-month period and will be paid to Coach on or before the end of the month in which the bonus vests.

3.11 Contingent Bonus: In the event the Coach continuously serves as the Program Head Coach through January 15, 2014, the University shall pay the Coach, on or before March 9, 2014, the amount of Two Million Dollars ($2,000,000).